Predictive Analytics for Debt Collection: Who to Call First

Predictive Analytics for Debt Collection: Who to Call First

Here is the everyday reality in most debt collection operations. You have a fixed number of agent hours, delinquency volumes that keep climbing, and a default playbook that quietly says "call everyone." So your team burns capacity chasing customers who would have paid on their own, while the borrowers about to slip into deeper buckets sit untouched in the queue.

The problem is rarely effort. It is sequencing and targeting. Calling the wrong customers first means your best hours are spent on your lowest-value contacts. This is exactly where predictive analytics changes the game. Instead of treating every overdue account the same, it decides who to contact, when, and on which channel, so finite agent time lands where it actually moves debt recovery. McKinsey found that an analytics-driven collections engine helped one bank lift cash collections by around 20 percent, and the wider shift is gathering pace: the AI debt collection market is projected to reach $15.9 billion by 2034. The opportunity is real, and it starts with smarter sequencing.

What Is Predictive Analytics for Debt Collection?

At its core, it uses historical data and customer behaviour combined with statistical and machine learning models to forecast which borrowers will pay, when, how much, and through which channel. That forecast lets collections teams prioritise effort instead of spreading it evenly across every overdue case.

The value is in scale. A human collector can read a handful of accounts well. No human can read patterns across hundreds of thousands of customers at once, spotting the subtle signals that separate a likely payer from a likely roll-forward. Machine learning models can.

It also helps to clear up a common confusion. Predictive analytics, artificial intelligence, and machine learning are not the same thing. Predictive analytics is the scoring brain that ranks your customers. Machine learning is the technique that powers that scoring and keeps it sharp. Conversational and voice AI is the engagement layer that acts on the score, reaching out to the right borrower in the right way. You need all three working together, but each plays a distinct role.

Also Read: What is Predictive Customer Support?

Descriptive vs Predictive vs Prescriptive: What's the Difference?

Most teams already do descriptive analytics without calling it that. The journey to better collections is moving from looking backward to acting forward.

Descriptive reporting tells you where you have been. Predictive scoring tells you where each customer is heading. Prescriptive analytics tells you what to do about it. Collections maturity is simply the climb from one stage of analytics to the next.

How Does Predictive Analytics Actually Work in Collections?

The models learn from signals you already collect. Repayment history, account age, outstanding balance, prior promise-to-pay behaviour, how responsive a borrower has been to past contact, which channels they engage with, and broader segment or macro data. Each customer leaves a trail, and the model learns which trails tend to end in payment.

From those signals, a few core predictive models do the heavy lifting. None of them require you to understand the maths. They just need to be pointed at clean data and connected to action.

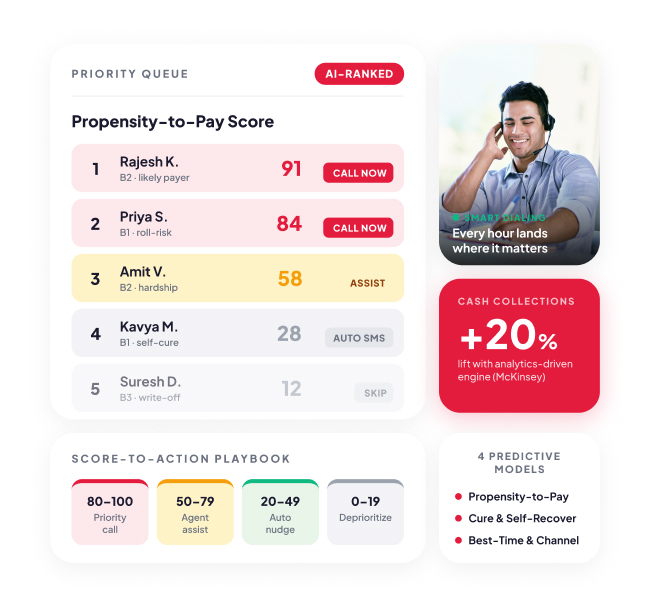

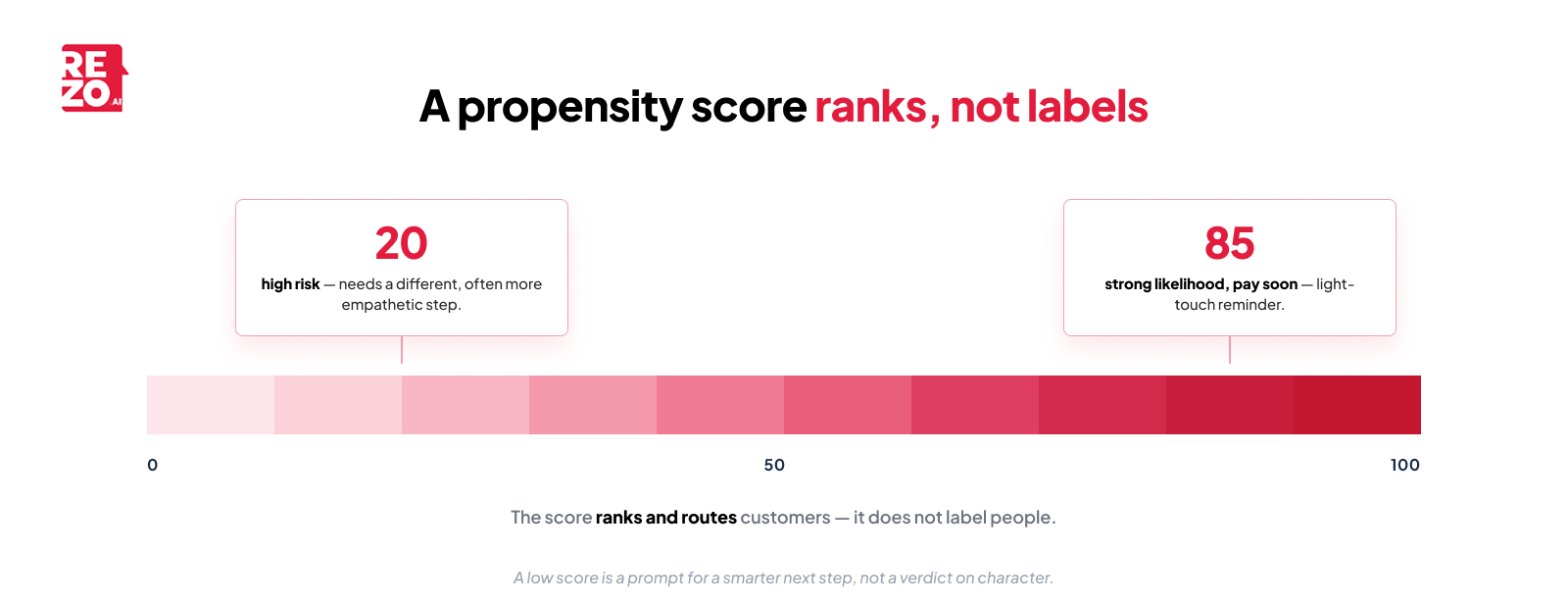

The Propensity-to-Pay Score

A propensity-to-pay score estimates how likely a customer is to repay within a given window, usually expressed as a probability or a band from 0 to 100. A score of 85 signals a strong likelihood of payment soon. A score of 20 flags a high risk customer who needs a very different approach.

Crucially, the score ranks and routes customers. It does not label people. A low score is not a verdict on a borrower's character. It is a prompt to choose a smarter, often more empathetic, next step rather than another wasted call.

Cure, Roll-Rate, and Re-Default Models

Three more predictive models sharpen the picture. Cure models flag delinquent accounts likely to recover on their own, so you stop spending calls on self-curers, a bigger group than most teams expect, since roughly 80 percent of customers cure within 30 days of delinquency. Roll-rate models flag customers likely to worsen into later, harder-to-recover buckets if left untouched, so you prioritise them now. Re-default models flag customers that have "recovered" but are likely to slip again, so you can keep a light, preventive touch on them.

Best-Time and Best-Channel Models

Knowing who to call is only half the answer. Best-time and best-channel models predict the optimal contact window and the right channel for each borrower, whether that is a voice call, WhatsApp, SMS, or email. This is what produces the "fewer contacts, higher connect rates" outcome so often cited. In high-volume retail lending, where borrowers are multilingual and spread across digital channels, matching the message to the moment is the difference between a connect and a dead dial.

Also Read: AI for debt collection

From Score to Conversation: How Prediction Drives Smarter Outreach

Most articles stop at the score. That is the wrong place to stop, because a score is worthless until it changes the conversation.

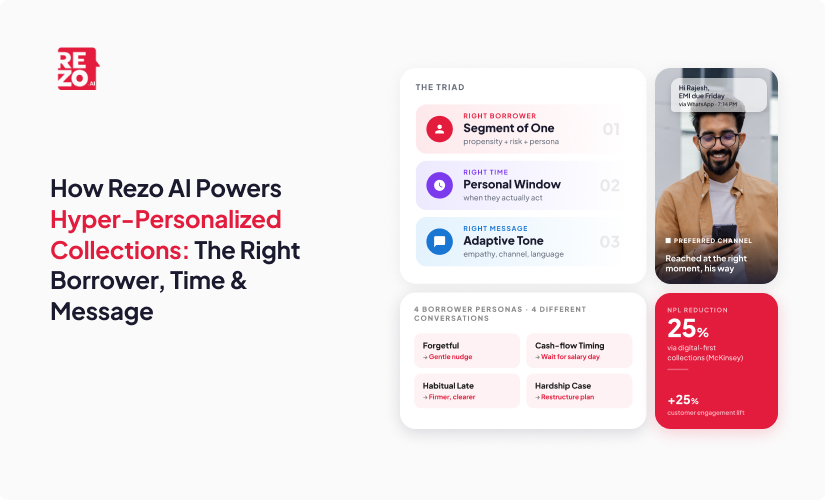

The real work is segmentation to action. A self-cure customer gets a light-touch reminder, not an agent call. AI tools can automate those payment reminders and case allocations, freeing agents entirely from the routine end of the queue. An agent-assisted customer, high value and responsive, gets a priority human call. A hardship case gets an empathetic conversation about restructuring rather than pressure. A low-priority or write-off-review account moves out of the active queue so it stops stealing attention.

The score sets more than who and when. It shapes the tone and the script. A likely self-curer gets a gentle nudge. A hardship borrower gets a flexible, respectful offer. This is where humanised, multilingual, omnichannel AI engagement fits. Predictive scoring routes routine customers to automated outreach and reserves your human agents for the high-value, sensitive negotiations where empathy and judgement actually matter.

Picture a lender with 200,000 delinquent accounts and far too few agents to call them all. Once scoring runs, perhaps 40 percent are likely self-curers who need only a reminder, a slice are clear hardship cases needing care, and a focused middle band is where human calls will move the most money. The headcount has not changed. The sequencing has, and that is what lifts recovery and protects your recovery rates.

Also Read: Hyper personalisation in Debt Collection

What Results Can You Expect?

The headline outcome is higher recovery rates from the same headcount, simply by sequencing the right customers first. When agents spend their hours on customers who genuinely respond to a call, every hour works harder, and automated planning can make the surrounding operations run up to 8 times faster.

You also see fewer wasted contact attempts and better response rates, which protects both agent capacity and borrower goodwill. Earlier intervention is another win. Roll-rate models surface customers heading for trouble before they become genuinely hard to recover, so you act while recovery is still likely. McKinsey reports that behavioural segmentation in collections has driven improvements of 20 to 30 percent in select segments. Experian similarly notes that predictive tools forecast repayment likelihood and help financial institutions prioritise high risk accounts and personalise communication.

There is a quieter benefit too. Borrowers stop getting bombarded with irrelevant calls and start getting contact that is timely and relevant. That experience matters for customer satisfaction, because a borrower treated well today is more likely to repay tomorrow. Done well, AI-driven strategies can enhance customer engagement and reduce operational costs at the same time.

How Do You Put Predictive Analytics Into Practice?

You do not need a big-bang transformation. The financial institutions that succeed roll this out in a deliberate, sequenced way, proving value on a small slice before scaling.

Step 1: Build the Data Foundation

Start by auditing and consolidating your repayment, account, and contact-history data. Fix the basics first, such as missing fields, duplicate records, and inconsistent formats, before any modelling begins, because a model is only as good as the data underneath it. Clean, well-structured data also helps reduce human error downstream. At the same time, define what success means up front, whether that is debt recovery rate, connect rate, or cost-to-collect, so you can measure progress honestly.

Step 2: Start With a Pilot Segment

Pick one high-volume, well-understood portfolio segment and run a champion versus challenger test. The challenger group gets predictive sequencing. The control group continues with business-as-usual outreach. Keep the pilot small enough to learn fast, but large enough to be statistically meaningful, so the results you see are real and not noise.

Step 3: Connect Scoring to the Action Layer

This is where many projects stall. Wire the scores directly into your routing, dialer, and omnichannel engagement so predictions actually change who gets contacted and how. Just as important, enable your agents with the score's context and a suggested next action, not a raw number on a screen they have to decode mid-call.

Step 4: Close the Feedback Loop

Feed real outcomes back into the model so it retrains and recalibrates over time, and monitor for drift as customer behaviour and the economy shift. This is what keeps decision making data driven rather than guesswork. Once the pilot proves out, expand to more segments with confidence. The loop is what keeps the system improving rather than slowly going stale.

Also Read: How Rezo achieved 40% Higher Recovery Rates in Debt Collection?

Is It Compliant and Fair? Using Predictive Analytics Responsibly

Predictive scoring has to respect data-privacy and fair-treatment obligations, which vary by region and sit alongside consumer-protection norms. Regulatory compliance is a top priority across financial services, so this is not optional, and it is not a reason to avoid analytics. It is a reason to do it well.

The biggest risk to watch is algorithmic bias that could unfairly disadvantage low-income or vulnerable borrowers. Remember the principle from earlier: models predict accounts, not character. Build in checks so the model is not quietly penalising people for circumstances rather than behaviour. Transparency, human oversight, and auditability are the safeguards here, and they help you meet regulatory requirements. Keep a human in the loop for sensitive decisions, and maintain explainability so you can show why a customer was treated the way it was. Deloitte's Trustworthy AI framework makes the same point, calling for AI that is fair, transparent, and accountable, with human oversight and a reliable audit trail.

Responsible use is also simply better business. Trust and fairness protect your brand, and a borrower treated with respect today is far more likely to be recoverable tomorrow.

The Bottom Line

The win in collections is not calling more. It is calling smarter. Predictive analytics decides who to contact first, when, and through which channel, so your finite agent hours land where they move the needle.

But the score alone is not the prize. The full value comes from joining prediction to humanised, omnichannel engagement, and from using it responsibly so trust and recovery rise together. Lenders who sequence intelligently will steadily out-recover those who keep dialing blindly through the list, turning data driven debt recovery into a durable edge.

If you are ready to stop calling everyone and start calling the right accounts first, book a consultation with Rezo.ai on predictive, AI-assisted collections.

Frequently Asked Questions

How much does predictive analytics for debt collection cost?

Costs vary widely, from subscription-based platforms billed per account or seat to custom-built predictive models. Beyond licensing, budget for data preparation, integration, and ongoing maintenance. Cloud and no-code tools have lowered the entry point, making predictive collections viable even for smaller lenders.

Can small debt collection agencies use predictive analytics?

Yes. You no longer need a data-science team or huge budgets. Cloud-based and no-code platforms let smaller agencies score customers using their own payment history. Start with a single high-volume segment, prove value, then scale, rather than buying enterprise infrastructure upfront.

How accurate is predictive analytics at predicting who will pay?

Accuracy depends heavily on data quality and volume, not the algorithm alone. Well-built models reliably rank customers by repayment likelihood, but they estimate probability, not certainty. Treat scores as prioritisation guidance, monitor for drift, and retrain regularly as customer behaviour and economic conditions change.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now