How Rezo AI Powers Hyper-Personalized Collections: The Right Borrower, the Right Time, the Right Message

How Rezo AI Powers Hyper-Personalized Collections: The Right Borrower, the Right Time, the Right Message

Most debt collection strategies still run on a simple, broken idea: contact everyone, the same way, at the same time, and hope enough of them pay. Hyperpersonalisation in collections flips that logic. Instead of one script and one 10 a.m. robocall for thousands of borrowers, artificial intelligence decides the right borrower to reach, the right time to reach them, and the right message to send, for each person individually. That shift is what separates lenders who recover more (while keeping borrowers on side) from those who burn goodwill chasing payments. Here is how Rezo AI makes hyper-personalized collections work at enterprise scale.

Why Traditional Collections Are Quietly Costing You Recovery

Delinquency volumes keep climbing, but debt recovery teams rarely grow at the same pace. The usual response is to do more of the same, faster: batch-and-blast SMS, dial-everyone campaigns, the same reminder script for every account. It feels productive. It quietly leaks recovery.

When every borrower gets the same channel and the same tone, you are treating a forgetful first-time late payer exactly like a habitual avoider or someone in genuine financial hardship. Those are three completely different problems, and a single approach gets all three wrong. The good-faith borrower feels harassed, the avoider learns to ignore you, and the hardship case shuts down entirely.

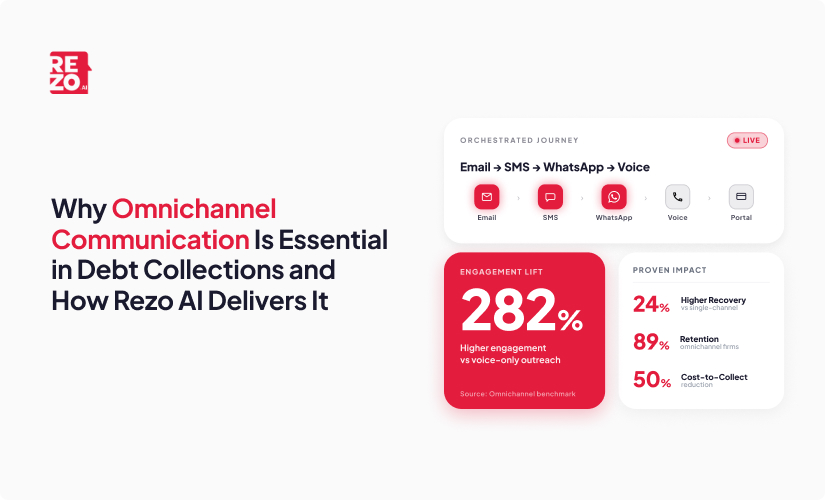

Channel choice alone moves the needle. McKinsey found that 58% of customers paid in full or part after an email, versus 48% after a collector phone call and 50% after a physical letter. Borrowers also notice when you do not know them. Salesforce reports that 73% of customers expect companies to understand their unique needs, while 56% say companies treat them as numbers; other research puts customer frustration with non-personalized experiences as high as 74%. Generic outreach does not just underperform; it erodes trust and raises compliance exposure. The fix is structural: the right borrower, the right time, the right message.

What Hyper-Personalization in Collections Actually Means

Hyper-personalization in debt collections is the use of real-time data, behavioral signals, and a combination of AI and machine learning to tailor who you contact, when, how, and with what tone, for each individual borrower rather than each broad segment. It is the practical core of any modern hyper-personalization strategy in lending.

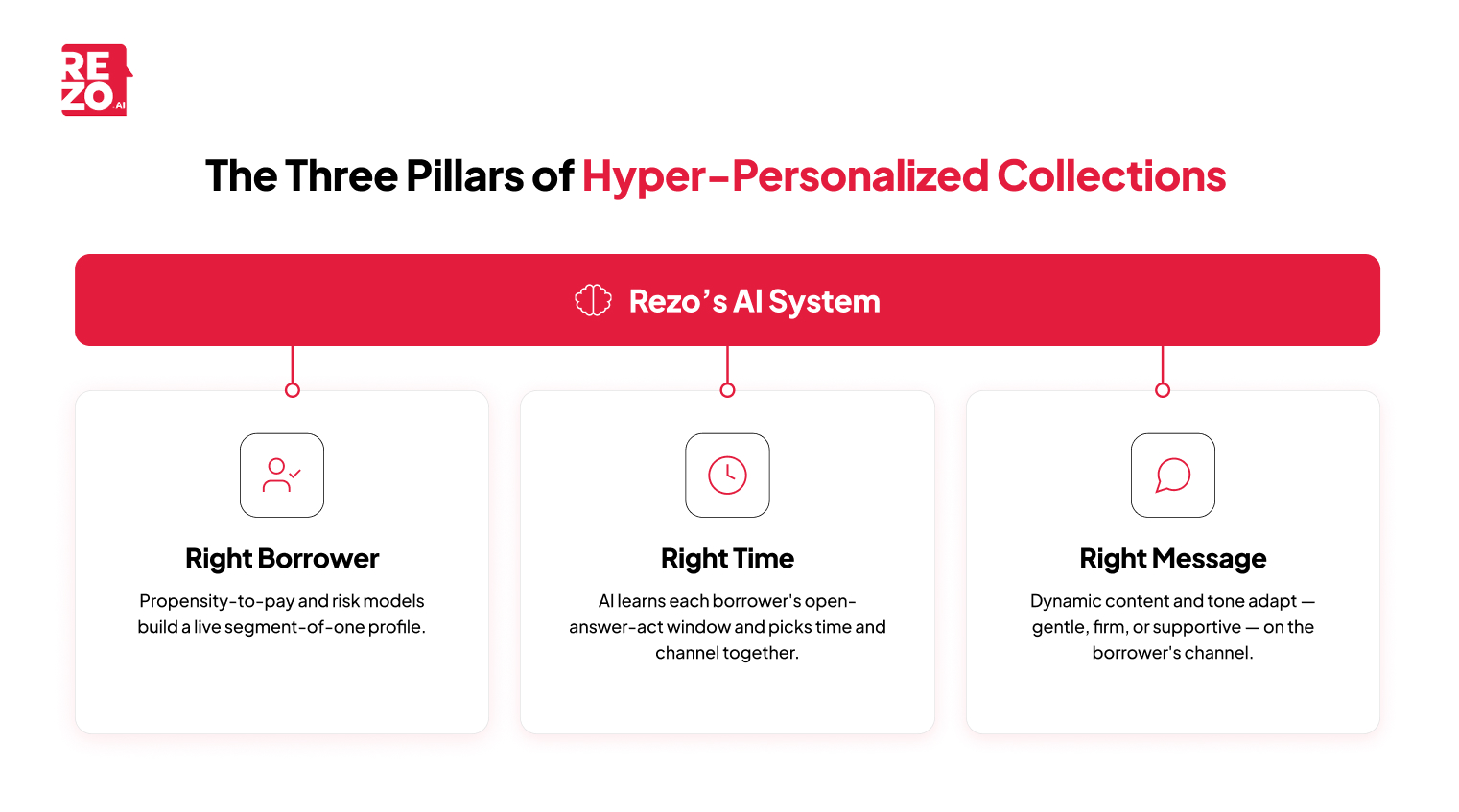

That last part is the key difference. Basic customer segmentation sorts borrowers into a handful of static buckets (30-day late, 60-day late, high balance) and treats everyone in a bucket the same. Hyper-personalization treats each borrower as a segment of one, a profile that updates continuously as new behavior comes in. It is the convergence of three things: prediction (propensity to pay and risk), decisioning (the next-best time and channel), and empathetic execution (the right message, delivered the right way).

This matters because personalized service is not a nicety in lending; it is a trust mechanism. Deloitte notes that more than half of bank customers say personalized service is key to trusting their bank, and hyper-personalization is how that service scales to every account. In debt collections, trust is what gets debts repaid, and it lifts both repayment and long-term customer satisfaction. The rest of this article breaks the approach into its three pillars: the right borrower, the right time, the right message.

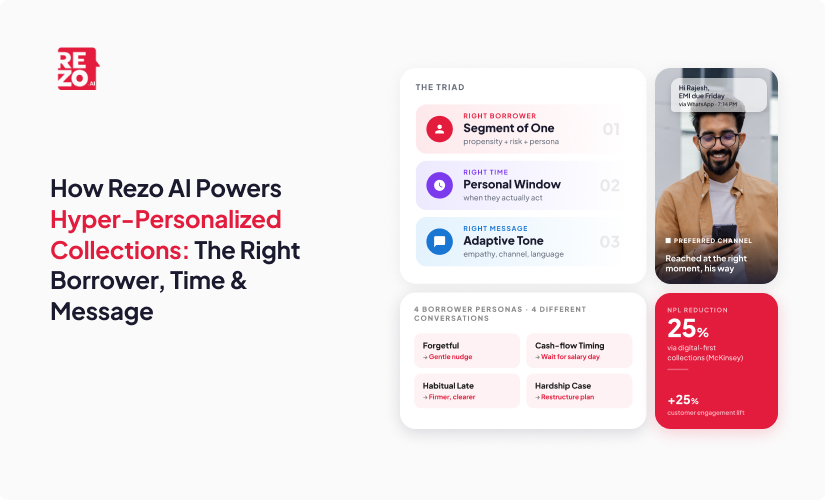

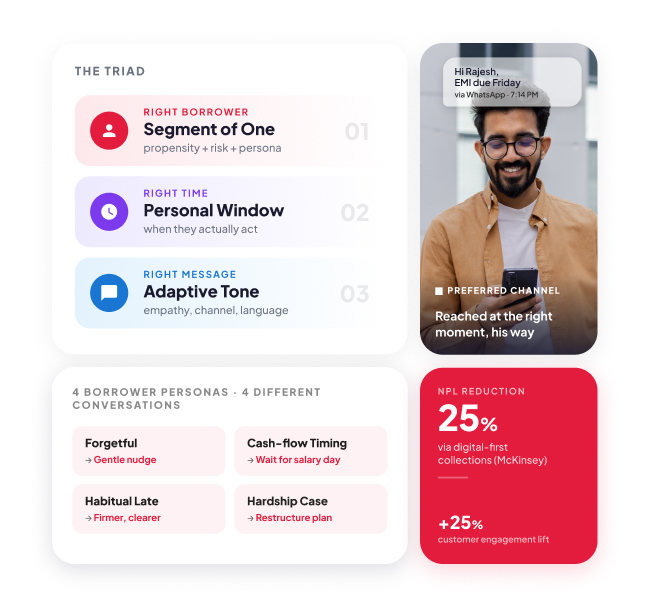

The Right Borrower: Knowing Who to Reach and Why They Are Late

The first pillar is understanding who you are actually talking to. Rezo AI builds a live borrower profile from real-time data: repayment history, transaction signals, prior customer interactions, channel responsiveness, and life-event cues. From that, propensity-to-pay and risk models predictive machine learning models trained on borrower behavior; rank borrowers so collection effort flows where it will matter most, instead of spreading thin across an undifferentiated list.

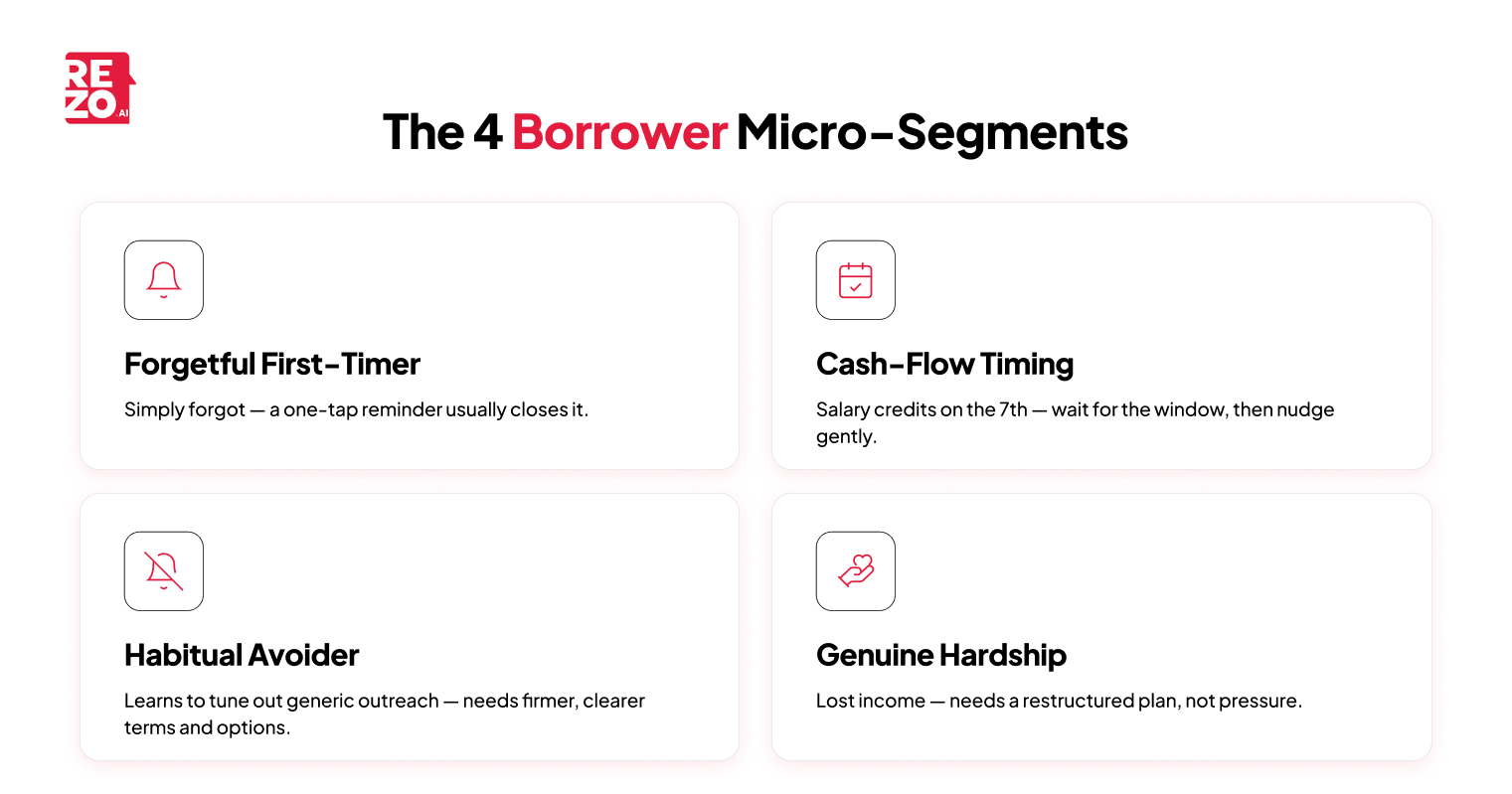

The real power is in behavioral micro-segments built from each borrower's behavioral patterns. The model distinguishes the forgetful first-time late payer from the cash-flow-timing case, the habitual late payer, and the borrower in genuine hardship. Each needs a different next action, and identifying which is which is half the battle.

From Static Buckets to a Segment of One

Picture two borrowers, both five days late on the same product. In a bucketed system they get identical treatment. In reality, one simply forgot and needs a one-tap reminder; the other has lost income and needs a restructured plan, not pressure. Same bucket, opposite right next action.

The highest-value move happens before anyone is even late. By reading early signals with predictive analytics, the system can flag a borrower at risk of a 30-day delinquency before the first missed payment and nudge them proactively. A borrower whose salary credits on the 7th should never be chased on the 3rd; wait for the window, and a gentle reminder often closes it with zero escalation. Based on customer behavior catching delinquency early, while it is cheap to resolve, is one of the most direct ways to pull down cost-to-collect.

The Right Time: How AI Picks the Moment Most Likely to Get a Yes

Knowing who to contact is wasted if you reach them at the wrong moment. Rezo AI uses real-time data to learn each borrower's individual pattern of when they open messages, answer calls, and actually act, then schedules contact inside that personal window rather than a fixed campaign calendar.

Timing and Channel Are One Decision, Not Two

How does AI choose the best time to contact a borrower? It treats timing and channel as a single decision. There is no point picking the perfect hour for a channel the borrower ignores. The AI system selects the best time on the best channel together, so the message lands when the borrower is most receptive and where they are most likely to respond. A WhatsApp nudge at 7 p.m. can convert a borrower who let a 10 a.m. call ring out every day that week.

Frequency is paced to avoid fatigue and to respect legal contact windows, so persistence never tips into harassment. And the system keeps learning: every contact, open, click, and payment feeds back into the next decision through continuous feedback loops. That compounding precision is why smarter timing and channels move real outcomes. McKinsey reports that generative AI can lift collector recovery outcomes by around 6%, and that digital-first collections can raise customer engagement by more than 25%.

The Right Message: Tone, Channel, and Empathy That Borrowers Respond To

The third pillar is what you actually say and how it feels to receive it. Rezo AI assembles dynamic, personalized content (the amount, due date, payment-plan options, and language) tailored to individual customer needs and channel preferences, then delivered on the borrower's preferred channel, whether that is voice, SMS, WhatsApp, email, or IVR. The result is personalized communication that reads as a one-to-one message, not a mass blast.

Tone adapts to context. A first-time miss gets a gentle, no-judgment reminder. A habitual avoider gets firmer, clearer language about consequences and options. A borrower in hardship gets supportive, solution-oriented messaging that opens the door to a manageable payment plan. Same goal, three very different conversations.

How Empathy Gets Engineered, Not Just Promised

Empathy in debt collections is often promised and rarely built. Here it is engineered. Real-time sentiment analysis listens for distress cues, a phrase like "I just lost my job" or rising frustration in a voice call, and routes that borrower out of standard pressure flows and into a hardship workflow or straight to human agents. The system recognizes when a script is the wrong tool.

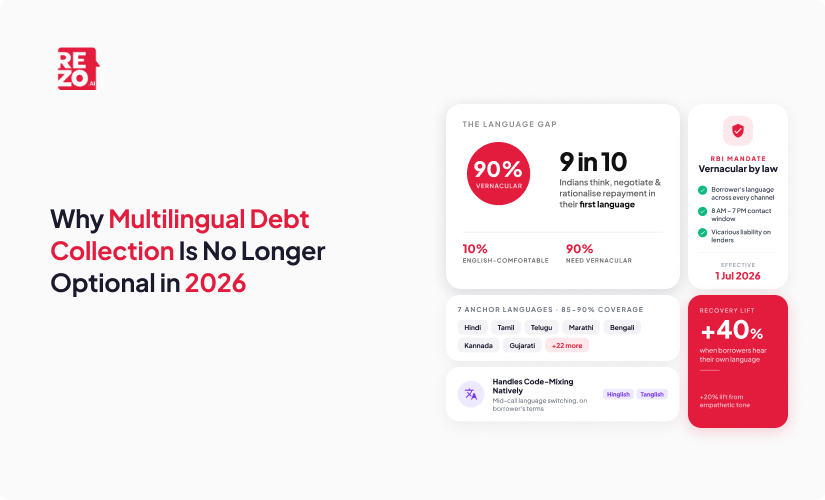

Language is part of the message too. For high-volume retail lending across India and other emerging markets, multilingual and vernacular outreach is decisive. One borrower might receive a vernacular WhatsApp message with a self-serve payment link and resolve it in seconds; another, flagged as distressed, gets an empathetic call from a trained human agent. Both feel understood, and personalized service is what builds the trust that ultimately gets debts repaid.

How the Agentic AI Behind Rezo Actually Works

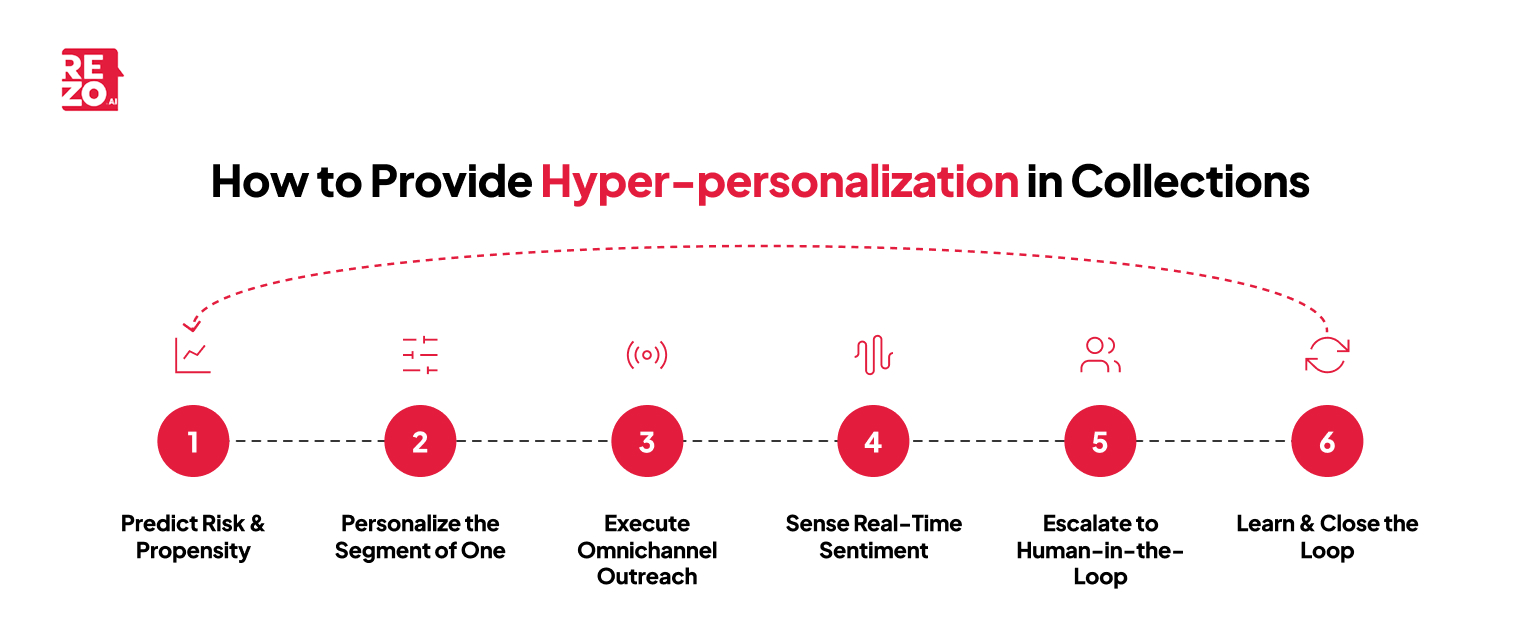

Underneath the three pillars sits a layered agentic system, built on AI agents that each own a stage of the collection process. The flow runs end to end: predict (risk and propensity), then personalize (the segment of one, message, and tone), then execute (agentic omnichannel outreach across voice, SMS, WhatsApp, email, and IVR), then sense (real-time sentiment), then escalate (human-in-the-loop), then learn (the feedback loop).

The word agentic matters. This is not a glorified message scheduler. The AI conducts actual conversations, negotiates payment plans within guardrails you define, and adapts mid-conversation when a borrower pushes back or volunteers new information. It acts, not just sends.

Crucially, humans stay in the loop. The AI handles early-stage and high-volume outreach plus agent assist, while human collectors own complex negotiations and sensitive cases, with human oversight on every high-stakes decision. That answers the "robots chasing debtors" objection directly: the goal is not to remove people, but to free them from repetitive, routine tasks so they can focus on the conversations that genuinely need human intervention. And because the loop closes on itself, every outcome makes the next contact smarter. To go deeper on the underlying approach, see Rezo AI's guide to AI in debt collection.

Is AI-Driven Collections Compliant? Compliance Baked In, Not Bolted On

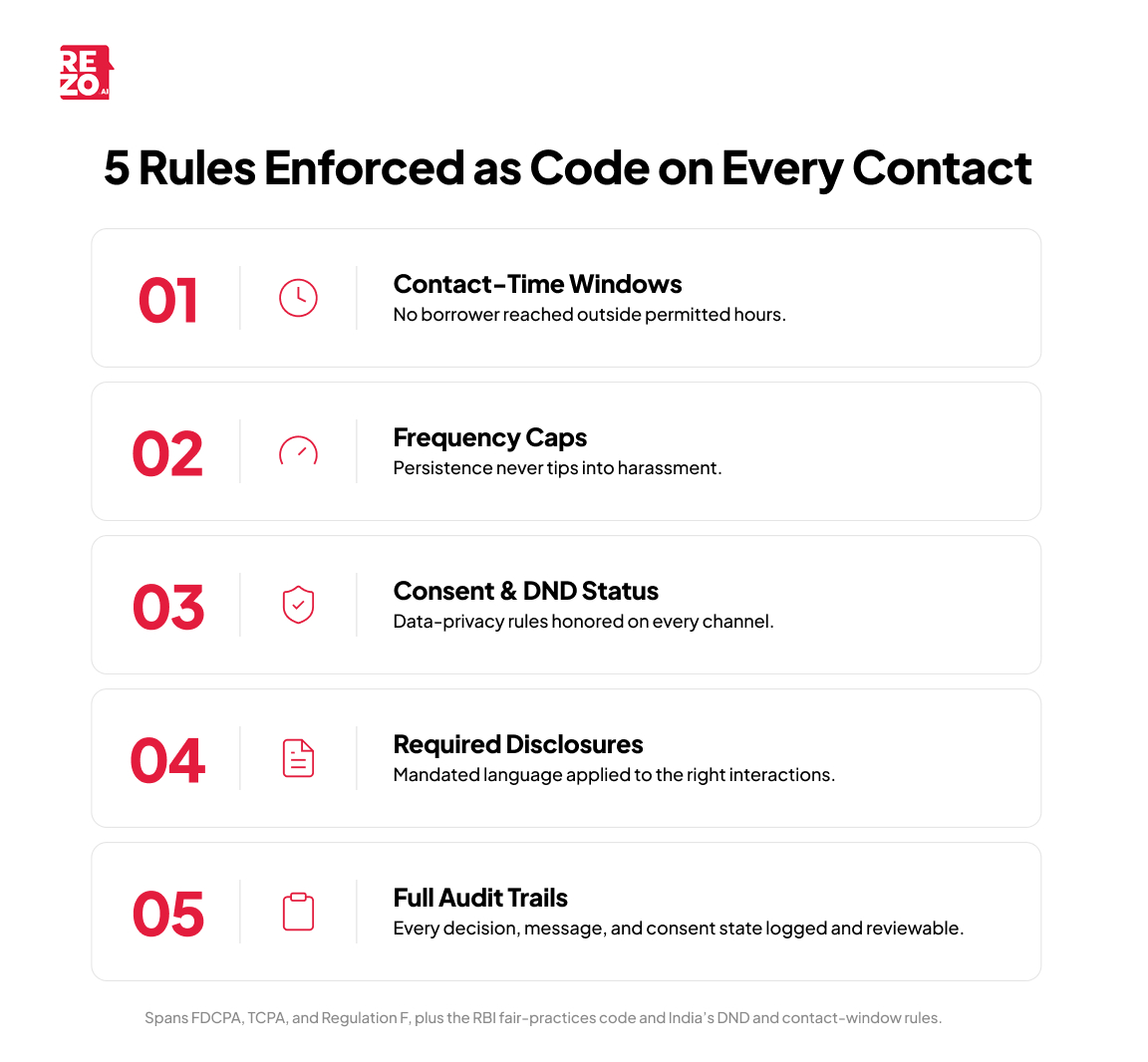

For BFSI leaders, this is usually the first real question. The honest answer is that AI-driven debt collection can be more compliant than manual operations, because the rules are enforced as code on every single contact rather than left to human judgment under pressure.

Compliance-as-code means the platform automatically enforces:

- Contact-time windows, so no borrower is reached outside permitted hours

- Frequency caps, so persistence never becomes harassment

- Consent and DND status, with data privacy rules honored on every channel

- Required disclosure language, applied to the right interactions

- Full audit trails, where every decision, message, and consent state is logged and reviewable

This spans FDCPA (the Fair Debt Collection Practices Act), TCPA, and Regulation F for US lenders, plus the RBI fair-practices code and India's DND and contact-window rules, the specifics that US and EU-centric vendors routinely overlook. The empathy and hardship routing described earlier do double duty here: by de-escalating distressed borrowers instead of pressuring them, they cut conduct and complaint risk at the source.

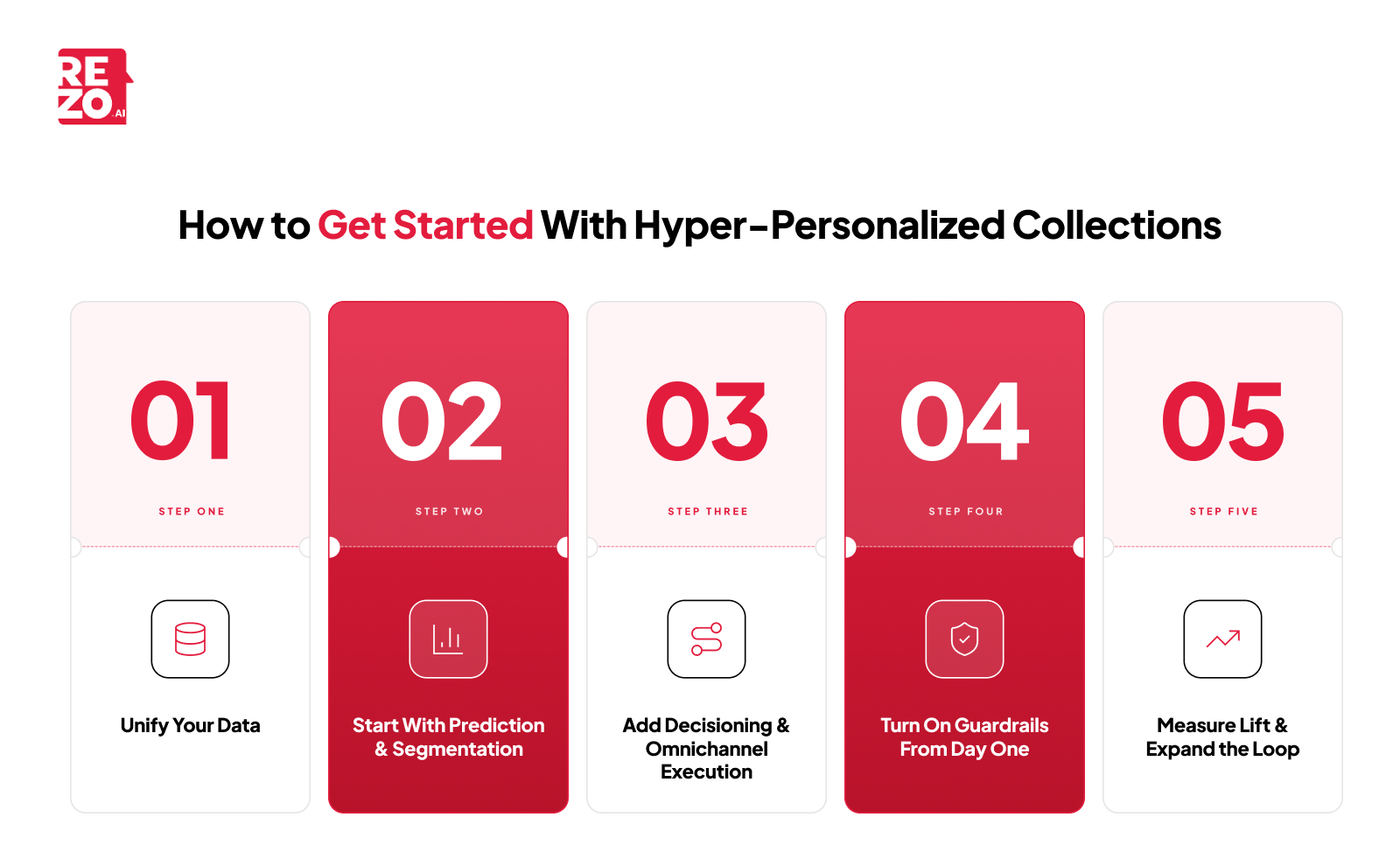

How to Get Started With Hyper-Personalized Collections

You do not need to rebuild everything at once. A practical hyper-personalization strategy rolls out in stages:

- Unify your data. Pull repayment history, contact logs, channel preferences, and consent state into one place. Clean customer data is the foundation everything else stands on.

- Start with prediction and segmentation on a single portfolio or delinquency bucket. Prove that scoring and micro-segmentation sharpen your targeting.

- Add next-best time and channel decisioning, then layer in agentic omnichannel execution across voice, SMS, WhatsApp, email, and IVR.

- Turn on compliance guardrails and human-in-the-loop escalation from day one. These are not phase-two features; they protect you from the first contact.

- Measure recovery lift, cost-to-collect, and engagement, then expand the learning loop across more portfolios.

A Phased Rollout That Proves Value Fast

Pilot your hyper-personalization efforts on one segment, measure hard, and expand on results. With only about 11% of debt collection firms using AI in 2023 (TransUnion), early movers still hold a real competitive advantage, and the benchmarks justify the move: McKinsey's work on digital-first collections points to 20 to 25% reductions in non-performing loans, meaningful cost takeouts, and more than 25% higher customer engagement, with one lender cutting average repayment time roughly fivefold. When you evaluate AI solutions, look for genuine agentic AI capabilities, true omnichannel reach, real-time compliance, multilingual voice, and audit-ready logging. If any of those are bolt-ons rather than core, you will feel it at scale.

Also Read : How Rezo AI Achieves 40% Higher Recovery Rates in Debt Collections Through Intelligent Automation

How Rezo AI Brings the Right Borrower, Right Time, Right Message Together

Rezo's AI Agents runs the entire predict-personalize-execute-sense-escalate-learn loop end to end, so the three pillars of hyper-personalization are not separate tools you stitch together but one system.

Map it back to the triad. The prediction and micro-segmentation layer delivers the right borrower. The next-best time and channel decisioning delivers the right time. The agentic, multilingual omnichannel execution across voice, SMS, WhatsApp, email, and IVR delivers the right message. Wrapped around all of it are real-time compliance guardrails and human-in-the-loop escalation, built for banks and financial institutions at BFSI scale from the start. The result is higher debt recovery, lower cost-to-collect and operational costs, improved customer satisfaction, and a borrower experience that protects customer relationships instead of damaging them. See how Rezo AI personalizes collections at scale. Book a demo.

Conclusion: Collections That Treat Borrowers Like People

The right borrower, the right time, the right message, delivered compliantly and empathetically at scale: that is the whole shift in one line. Hyper-personalization moves collections from chasing debtors to engaging borrowers with personalized experiences, and the lenders who make that move recover more while keeping the relationship intact. When you are ready to see it in action, Rezo AI is built to take you there.

Frequently Asked Questions

Q1: What data does AI use to personalize debt collections?

AI draws on repayment history, transaction and cash-flow signals, prior interaction outcomes, channel responsiveness, consent and DND status, and life-event cues. This customer data feeds propensity-to-pay and risk models that build a continuously updating borrower profile, enabling per-individual decisions on who to contact, when, and how.

Q2: How do you measure the ROI of AI in collections?

Track recovery-rate lift, cost-to-collect reduction, non-performing-loan (NPL) movement, contact-to-payment conversion, and engagement or response rates. Pilot on one portfolio, set a baseline, and compare against it. McKinsey links digital-first collections to 20 to 25% NPL reductions and over 25% higher engagement.

Q3: What is the difference between digital-first and traditional collections?

Traditional debt collection leans on outbound phone calls and uniform batch outreach. Digital-first collections prioritize borrower-preferred digital channels (SMS, WhatsApp, email, self-serve links) with AI-driven timing and self-resolution. It lowers cost-to-collect, improves customer experience, and meets borrowers where they already prefer to transact.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now