The Empathy Bottleneck: How Manual Collections Forces Agents to Choose Between Speed and Care

The Empathy Bottleneck: How Manual Collections Forces Agents to Choose Between Speed and Care

NBFCs, BFSIs, and financial institutions have always had collections as one of their most high-volume use cases. And the numbers back it up. The global debt collection software market was worth around 5 billion dollars in 2025 and is projected to reach nearly 9 billion by 2030.

However, it is not all just numbers. In India especially, debt collections are not just about making a call and recovering debt. It is a delicate matter of customer experience, with customers coming from all backgrounds and levels of diversity. And a single, one-size-fits-all approach often leads to a negative experience, one that is not just limited to how the borrower feels about that institution, but also how they will feel about loans and debt going forward in their lives.

Why Empathy Matters in Debt Collections?

Debt collection calls occur when a borrower has failed to repay their debt or has missed instalments. But it is not always negligence. Sometimes, it is due to a medical emergency, delayed salary, job loss, business disruptions, or financial stress. Human agents working on a strict 9-to-5schedule often call these borrowers at their most financially vulnerable moments. And in these moments, the quality of engagement and the empathy shown matter.

Empathy in debt collections is not just a soft skill that agents need on their resumes. It is a factor that directly affects borrower responsiveness, repayment cooperation, long-term trust, and overall customer experience.

However, empathy often struggles to survive within traditional collections operations. Not because agents lack compassion, but because manual debt collections rarely give agents the time to practice it.

Empathy isn't a soft skill for an agent's resume; it directly drives borrower responsiveness, cooperation, and long-term trust.

Why Scaling Disrupts Modern Collections?

As discussed earlier, the collections market is expanding at a fast pace. However, with increasing lending penetration, rising customer volumes, and expanding credit ecosystems, there is enormous pressure on collections teams to handle higher outreach volumes with greater efficiency.

Agents are expected to manage large numbers of delinquent accounts, make high volumes of outbound calls daily, follow strict recovery timelines, maintain compliance standards, and aggressively meet targets. In all this, handling emotionally charged conversations often becomes increasingly difficult. Borrowers, on the other hand, expect personalized and instant responses, similar to what they receive from more customer-facing organizations.

Why Empathy is Inconsistent in Traditional Collections?

Agents are always on a time crunch, with a long list of delinquents to call and targets to achieve. A meaningful borrower interaction would require an agent to invest time, understand context, listen to the borrower, and possess the emotional bandwidth necessary to show empathy.

However, with piling defaulter lists and mounting targets, even experienced and capable agents find themselves stuck at a crossroads: either move fast enough to close calls or slow down and engage with borrowers meaningfully. And with agents being evaluated primarily on call volumes, PTP conversions, and overall efficiency, the first option is often chosen.

Add to that the burnout agents experience from difficult conversations, pressure-driven targets, and repetitive workflows, and empathy often takes a back seat.

Can Both Empathy and Efficiency Be Achieved?

As important as empathy is, if agents start spending significantly longer on each debt collection call, it could cause tremendous disruptions within the collections industry. Institutions would either be unable to sort through delinquency lists on time or would need to significantly increase their workforce to accommodate the volume.

However, neither of these approaches is sustainable or profitable. This is where conversations around AI agents come in not as a replacement for human agents, but as a way to remove operational burdens that prevent empathy from scaling effectively.

The goal isn't to replace human agents. It's to remove the operational burdens that prevent empathy from scaling.

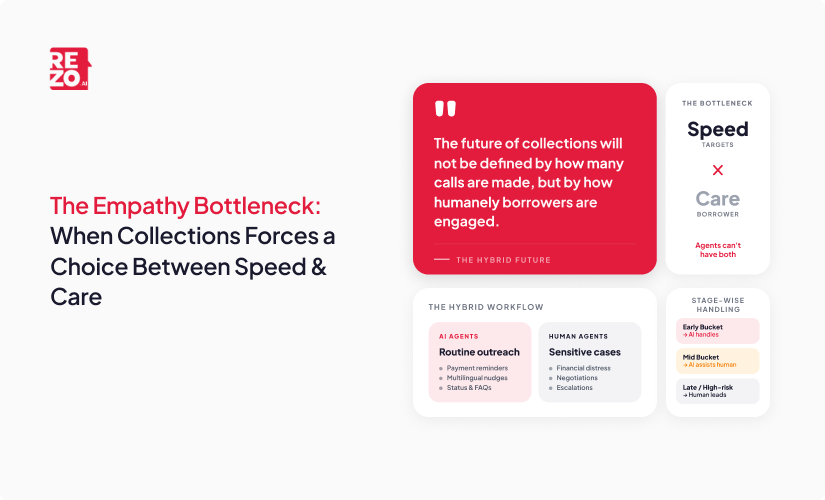

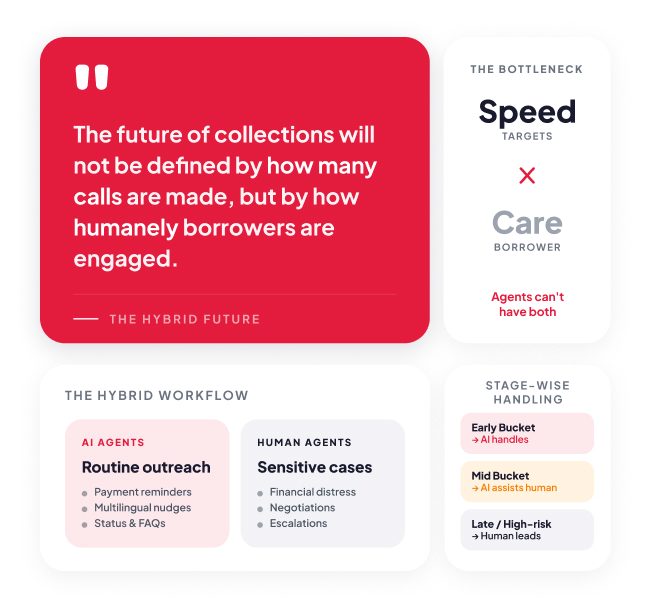

The entirety of collections cannot be automated, and that is true. However, by leveraging AI agents, a more hybrid workflow can be achieved, where human agents are utilized for more complex cases while AI agents handle repetitive queries. With this approach, both empathy and efficiency become possible.

How Agentic AI Reimagines Collections?

Not every stage requires the same level of human involvement. In the early stages of delinquency buckets, borrowers simply need timely reminders, repayment nudges, flexible payment options, or multilingual support. These interactions are repetitive, usually involve higher volumes, and are operationally heavy.

Agentic AI-powered agents can completely automate this outreach, freeing up a significant portion of human agents’ workload. These AI agents drive omnichannel support across WhatsApp, SMS, chats, and other communication channels while maintaining context and personalization through out the experience.

This allows financial institutions to increase outreach consistency, improve borrower responsiveness, reduce agent workload, and maintain engagement at scale.

As delinquency increases, borrowers require more nuanced and specific outreach campaigns. Mid-stage collections call for greater contextual understanding, repayment negotiations, multiple nudges, and intent-based engagement strategies. Here, AI agents can provide human agents with summaries of borrower history, identify risk signals, prioritize accounts to target, and maintain continuity across conversations and channels. Voice AI agents with human-like features can also be deployed for repeated reminder calls to delinquents.

In later-stage or high-risk buckets, where conversations involve financial distress, escalations, or sensitive negotiations, human agents become extremely important. Here, Agentic AI can work in a supporting role, assisting agents during collection calls.

With this approach, human agents are no longer overwhelmed by huge call volumes or repetitive workloads. Therefore, instead of picking and choosing where to display empathy, they can focus on more sensitive cases and dedicate more time to them, while AI agents handle the more general cases.

Instead of picking and choosing where to show empathy, agents can give the most sensitive cases the time they deserve.

What Does the Future Say?

Collections as a use case is undergoing a fundamental shift. Historically, the industry optimized primarily for recovery rates. But with the growing market, collections now need to be optimized for borrower engagement quality, contextual intelligence, and sustainable long-term relationships.

This shift matters not only for customer experience, but also for business outcomes. Borrowers are more likely to engage when communication feels respectful, contextual, and non-adversarial. Agents perform better when they are not under constant pressure.

Organizations benefit from a hybrid structure through stronger recovery rates, lower agent burnout, and more resilient borrower relationships.

The aim is not to blindly automate collections. It is to remove the operational bottlenecks that have made empathy difficult to sustain at scale.

The future of collections will not be defined by how many calls are made, but rather by how intelligently and humanely borrowers are engaged.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now