How Agentic AI Is Transforming Multilingual Gold Loan Servicing for Regional Lenders

How Agentic AI Is Transforming Multilingual Gold Loan Servicing for Regional Lenders

Gold loans have quietly become India's second-largest retail credit product, and the next wave of growth is not going to come from metros alone. It is going to come from Salem, Warangal, Nashik, Muzaffarpur, and hundreds of towns where a borrower walks in expecting customer service in their own vernacular language. For regional lenders, that is both the opportunity and the operational headache. Agentic AI for multilingual gold loans is the layer that makes it possible to grow without hiring a call centre in every dialect.

This piece is written for CX, operations, and technology leaders at regional NBFCs, co-operative banks, and small finance banks who are scaling gold loan books across South, West, North, and East India. We will walk through what agentic AI really means for gold loan servicing, why the language gap hits regional lenders first, how the full lifecycle can be handled in vernacular languages across voice, WhatsApp, and chat, how to align with RBI expectations, and a realistic rollout path that does not disrupt the branch.

Why Multilingual Gold Loan Servicing Is a Bigger Problem Than It Looks?

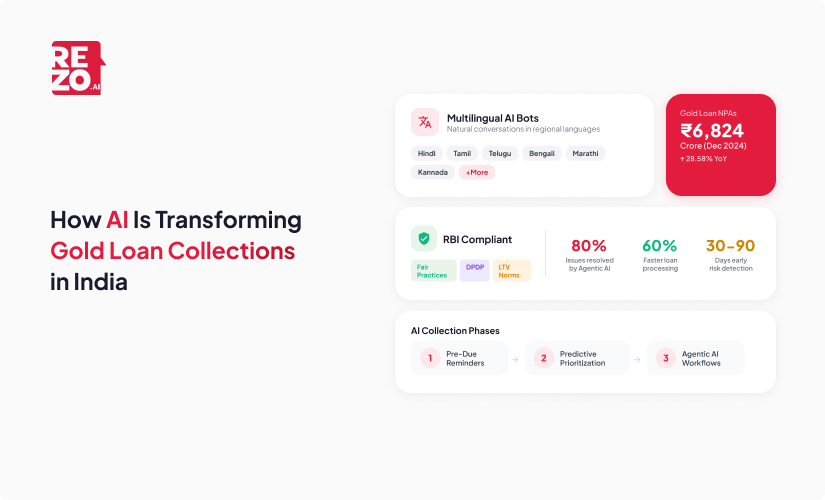

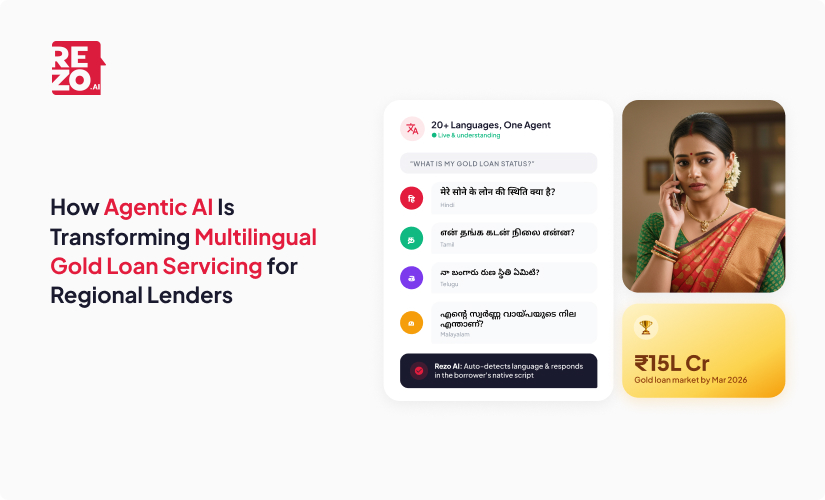

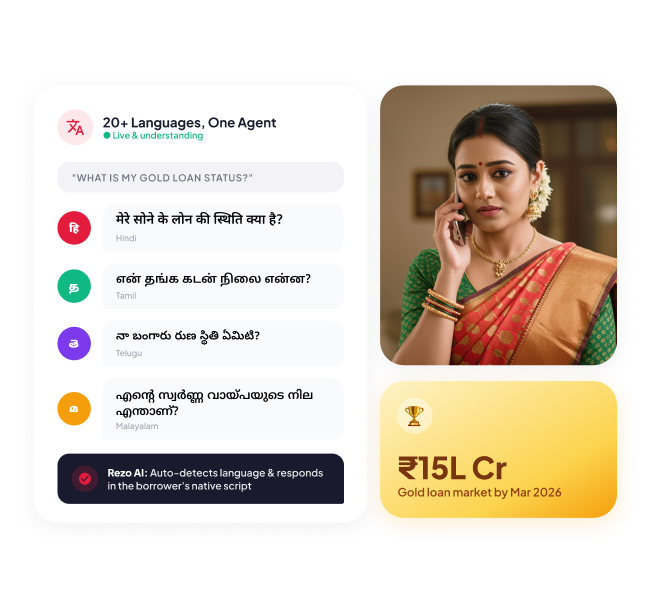

India's organised gold loan AUM is on track to cross Rs. 15 lakh crore by March 2026, according to ICRA's widely reported projection. Public sector banks still dominate, but NBFCs and small finance banks have been picking up share as customers shift toward formal, transparent lenders. TransUnion CIBIL has noted that gold loan balances have grown 3.8 times since March 2022, moving the product up to the second-largest retail credit category in the country.

The customers behind that growth are not uniform. A gold loan customer in Coimbatore speaks Tamil as their native language, prefers WhatsApp for pledge status, and expects a call back within the hour. A customer in Nagpur is comfortable in Marathi and Hindi, often code-switching mid-sentence. In Kochi, Malayalam is non-negotiable. A regional lender with a hundred branches across four southern states is effectively running four or five languages in parallel across extended customer service hours, and branches and tele-calling teams cannot scale linearly with that kind of AUM growth, especially when gold price movements trigger sudden spikes in renewal and LTV queries.

The stakes for language are not abstract. A global survey by CSA Research of 8,709 consumers across 29 countries found that 76% prefer to buy products with information in their native language, and 40% will never buy from websites in other languages. The number is even sharper for credit products where trust is load-bearing. A borrower who does not feel understood in her own language simply walks to the next lender, and that language barrier is often the difference between a renewal and a run-off.

How does Agentic AI enable Multilingual Support for Borrowers?

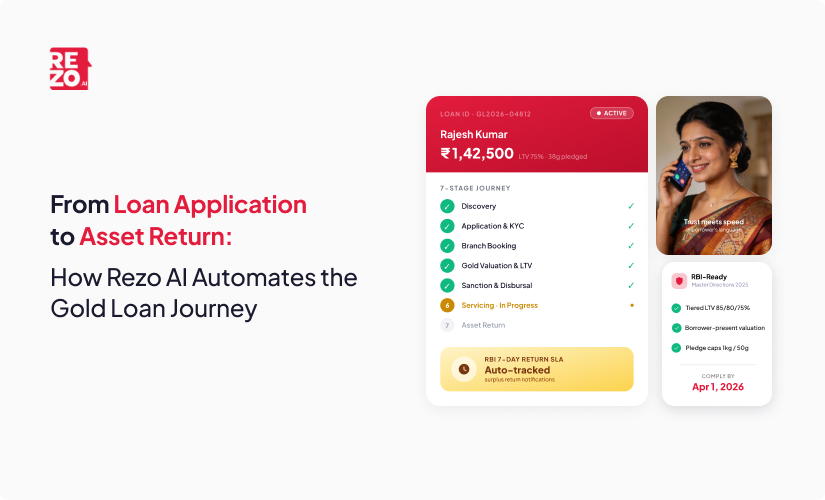

Agentic AI is not a rebranded chatbot. A traditional IVR plays menus. A rule-based chatbot answers single-turn questions. Agentic AI plans, decides, and acts across multi-step tasks, working with live customer data and taking the next best action on behalf of the borrower or the lender. It operates as a network of autonomous agents that manage the entire loan lifecycle in a preferred regional language, rather than a single bot bolted onto a website.

In a gold loan context, that means a single agent can authenticate a customer, pull the pledge record, quote current interest accrual, offer a partial release option, schedule a branch visit, send a WhatsApp confirmation, and log the entire interaction into the loan management system. All in the customer's regional language, without switching to any default language(English). Modern AI systems can automatically detect the customer's language from the very first message, so there is no clunky "press 1 for Hindi" menu standing between the borrower and her answer.

Gartner has publicly projected that by 2029 agentic AI will autonomously resolve 80% of common customer concerns without human intervention, and that banks deploying this approach to orchestrate workflows will outperform peers on operational efficiency by up to 35% by 2026. For regional lenders with tight operating ratios and thin margins, that is not an incremental gain. That is the difference between growing and getting outgrown. For a deeper view on the voice channel specifically, our earlier piece on AI voice bots in banking lays out how voice AI agents are already changing the frontline.

Why Regional Lenders Feel the Language Gap First?

Large banks and Fintechs can get away with English-first servicing because their customer base skews urban and digital. Regional lenders cannot. The gold loan customer profile is overwhelmingly semi-urban and rural, and the support experience stands or falls on the first two sentences a borrower hears in her own language.

A few patterns keep showing up in the field:

- Borrowers in Tier 2 and Tier 3 markets disengage quickly when the voice on the other end is English-only or over-formal Hindi, which turns routine phone calls into language barriers rather than resolutions.

- Code-mixed speech like Hinglish, Tanglish, and Manglish is the default in urban and semi-urban India, and older IVRs simply cannot parse it, which pushes basic support tickets straight to a human queue that is already stretched.

- Branch queues stretch every time gold prices move sharply because LTV rebalancing and renewal conversations spike at the same time across different languages and channels.

- Region-specific tele-calling teams are expensive to hire, hard to retain, and inconsistent on compliance, especially when shifted across states. Annual attrition for this kind of role regularly runs as high as 60% in parts of the industry, which means the language proficiency built up over months walks out the door every quarter.

- Brand voice and tone are hard to hold steady when native speakers across four or five teams interpret the same script differently, so the customer experience drifts from one region to the next even when the underlying product is identical.

The result is a servicing experience that looks fine on paper but bleeds customers at the margins, especially during renewal windows when retention matters most.

How Agentic AI Enables Multilingual Support in the Full Gold Loan Servicing Lifecycle?

Most conversations about AI in lending still default to collections. That is where the early wins came, and that is still a strong use case. Our earlier deep dive on AI in gold loan collections covers that territory in detail. But the real value of this technology for gold loans shows up across the lifecycle, not just at the recovery end.

Here is what a multilingual agentic AI layer can realistically cover today:

- Onboarding and KYC handholding: AI agents guide first-time borrowers through document collection in their preferred language, use AI-powered OCR to extract and validate data from varied documents regardless of scan quality or language, and analyse images of gold ornaments to estimate purity, karat, and weight before the customer even reaches the counter.

- Pledge status and interest queries: Real-time answers on outstanding principal, interest accrued, and next due date, pulled live from the LMS. The system also calculates the current loan-to-value ratio against live gold market prices, so the borrower gets a clear picture on demand.

- Renewal and top-up nudges: Price-triggered outreach when gold prices move enough to unlock a top-up or require a renewal conversation. AI-powered translation tools ensure the message lands naturally in the customer's language, not as a robotic machine-translated script, and generative models preserve context and idiom in a way older AI translation services could not.

- Partial release guidance: Walk a borrower through partial release mechanics, quote the revised EMI, and book the branch slot without a handover.

- EMI and interest collection: Empathetic outreach with tone calibrated by overdue bucket and borrower sentiment. Automated reminders sent in regional languages have been shown to lift repayment rates, because the borrower actually understands what she owes and by when.

- Auction notices: Consistent, compliant delivery of auction notices in the customer's language, with clear cure paths that reduce disputes downstream.

- Grievance intake: Sentiment-aware grievance logging that routes to human agents in the branch, contact centre, or ombudsman flow when needed.

- Fraud and risk signals: Agents can spot fake gold pledges or suspicious borrower histories in real time by cross-referencing behavioural fingerprints, and flag or freeze anomalous activity before it becomes a loss.

The orchestration across voice calls, WhatsApp, chat, and email is what makes this different from bolting a chatbot onto a website. A borrower can start a conversation on WhatsApp in Telugu, get a call back on voice, receive a confirmation SMS, and pick up the same thread the next day without repeating herself.

From Collections to Proactive Servicing

The shift is from reactive to proactive. Instead of waiting for the borrower to call, the system watches signals, LTV thresholds, renewal windows, interest accrual spikes, sentiment in past calls, and reaches out before a problem becomes a default. Predictive models assess repayment probability by analysing behavioural data and, for agri-heavy portfolios, regional cropping cycles, so outreach aligns with when the customer actually has cash in hand. For a broader view on how this plays out across the recovery book, see our piece on AI in debt collection. For regional lenders, that is how a gold loan book compounds without compounding the branch headcou

Why Vernacular Depth Matters More Than Vernacular Claims?

Most "multilingual support" claims in the market mean "we support ten languages in a dropdown". That is not enough for gold loan servicing. Multilingual customer support refers to a lender's ability to actually offer support across different languages so customers can communicate in their preferred language end to end, not just pick one from a menu. Vernacular depth is the difference between a borrower hanging up in thirty seconds and a borrower renewing for another cycle.

Three dimensions matter:

- Dialect variance within a state: Kongu Tamil sounds different from Madurai Tamil. Marathwada Marathi differs from Pune Marathi. A support agent that is trained on one and deployed across the other loses trust immediately, and no amount of generic translation services fixes that.

- Code-mixing as default: Urban and semi-urban speakers switch between English and the regional language mid-sentence. Conversational AI needs to understand and respond naturally in both, and modern generative models have made a real leap here by picking up context, idioms, and intent rather than translating word by word. That is what turns real time translation tools from a novelty into genuine native language support.

- Cultural nuances in gold conversations: Gold is emotional collateral. It is tied to weddings, education, medical emergencies, and inheritance. Tone has to adjust across renewal, collection, and grievance contexts, in the borrower's own idiom, which is why cultural training for the humans who review and refine these agents matters as much as the model itself.

Leading platforms already support conversations in regional languages and local dialects, which is what makes support in multiple languages a practical reality rather than a slide-deck promise. For a lender with a diverse customer base across four or five states, that kind of language-specific support is the clearest competitive advantage on the table.

How Agentic AI Aligns With RBI and Fair Practices Expectations?

Compliance is non-negotiable in gold lending, and the RBI's Fair Practices Code on recovery and customer communication applies fully to AI-driven outreach. A well-designed multilingual support system for gold loan servicing builds regulatory compliance into the workflow rather than bolting it on, with agents automatically enforcing the guardrails that tele-callers often have to remember manually.

The guardrails that matter for regional lenders:

- Consent-aware outreach with clear opt-in and opt-out paths for every customer.

- Automatic enforcement of time-of-day and call-frequency controls aligned with RBI and fair practices norms, so call-window restrictions are never breached in any language.

- Full recording and searchable transcripts in every supported language, available for audit, with sentiment analysis layered on top to identify risky conversations early.

- PII handling and data localisation aligned with Indian data protection expectations.

- Auction notice flows that follow the documented process and timeline required under the code.

- Real-time fraud prevention that monitors transaction patterns and can autonomously flag or freeze suspicious pledges the moment the pattern is identified.

Advisory voices have consistently flagged governance as the single biggest determinant of agentic AI success in financial services. Platform should make compliance easier for the audit team, not harder. You can read more in our AI governance article.

How to Roll Out Multilingual Agentic AI Without Disrupting Branches?

A common fear in regional lender boardrooms is that AI will collide with the branch model. It should not, if the rollout is phased correctly. A hybrid approach that pairs AI efficiency with human expertise, especially for effective multilingual support, is what makes this sustainable, allowing routine queries to flow through the agent while complex or sensitive issues are escalated to human agents. Here is a realistic path that CX and operations leaders have used to move from pilot to scale.

- Pick one high-volume flow first: EMI and interest reminders or renewal nudges are usually the cleanest starting points. They are high-volume, repetitive, and language-sensitive.

- Start with the top two borrower languages: Do not try to launch in ten languages on day one. Analyse your customer data to identify language priorities, pick the top two or three languages that cover the majority of your AUM, and get them right before adding the next.

- Integrate through APIs, not rip-and-replace: Connect the agentic layer to your existing loan origination and loan management systems, CRM, and telephony so the system of record stays where it is. With the right OCR and decisioning in place, parts of the journey can drop from days to minutes, with some automated flows turning around in 10 to 12 minutes end to end.

- Define handover rules to branches and tele-callers: The agent handles the routine. Branch and tele-calling teams handle sensitive grievances, high-value top-ups, and anything that requires a human touch. Draw the line clearly.

- Set up a vernacular QA cell: Quality analysts who are native speakers of each target language should score a sample of conversations every day, run sentiment analysis on edge cases, and feed corrections back into the agent so language proficiency improves rather than drifts.

- Scale language by language, use case by use case: Once the first flow is hitting connect-rate, containment, and compliance targets, add the next language or the next flow.

- Keep humans in the loop where it counts: Edge cases, sensitive grievances, and hardship conversations should always have a clear path to a trained human.

What Good Looks Like in the First Phase Rollout?

By the end of first phase, a regional lender should have one flow live in two languages, a clear SLA with the branch and tele-calling teams, and a daily quality scorecard. Early signals to look for include improved connect rate, higher containment in the automated flow, and a reduction in average handle time without a drop in customer satisfaction.

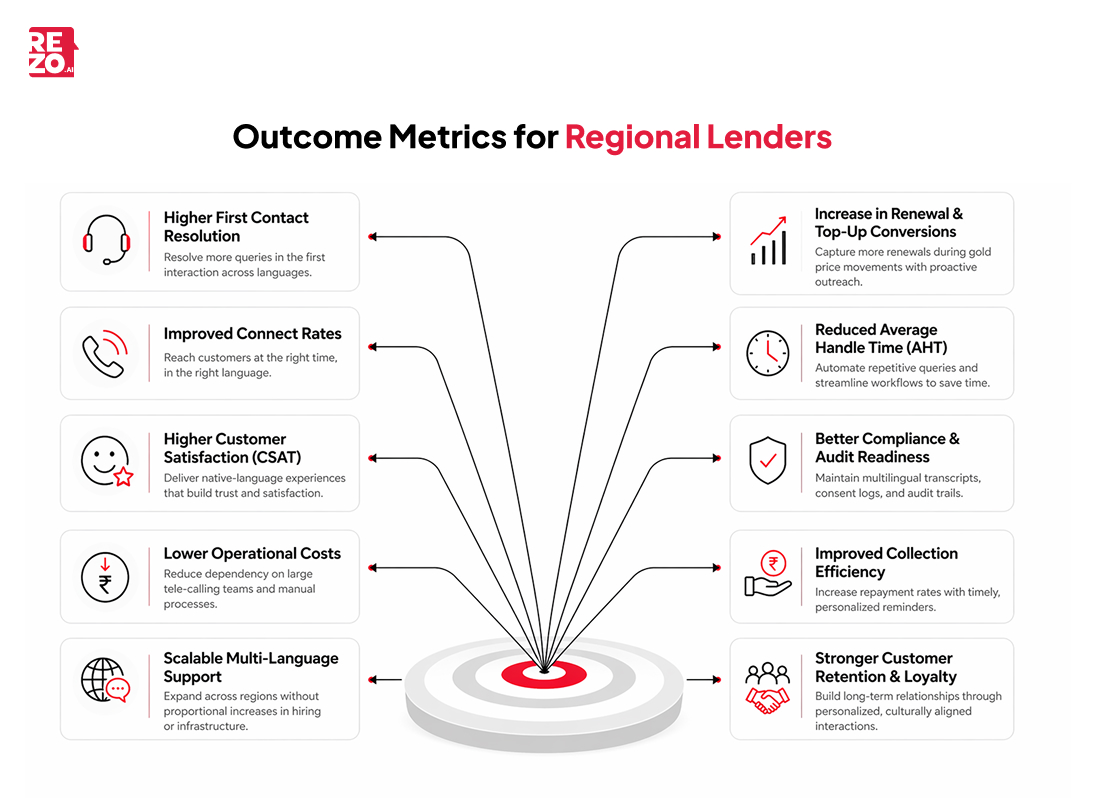

What Regional Lenders Can Expect as Outcomes?

Agentic AI does not replace the branch, and it does not replace the relationship manager. What it does is let a regional lender punch above its weight in languages, channels, and hours, and that is increasingly the competitive advantage that separates growing books from stagnant ones.

In practical terms, lenders who move early tend to see:

- Higher first-contact resolution across different languages, driven by consistent, trained AI agents that sound the same irrespective of which region the borrower is located in.

- Better connect rates and intent qualification, because outreach happens at the right time and in the right language for each customer.

- Stronger renewal and top-up capture during gold price swings, because the system reaches borrowers proactively in their preferred language instead of waiting for them to walk in.

- Lower dependence on region-specific tele-calling teams, which frees up budget for frontline branch talent and removes a chronic hiring headache.

- A measurable drop in operating costs. Automating routine tasks can significantly reduce operational costs in NBFCs, particularly for processes that are repetitive and well-suited to automation. At the same time, AI-driven KYC and document verification are accelerating approval timelines, enabling faster decision-making and improving overall operational efficiency.

- Cleaner multilingual audit trails that make Fair Practices Code compliance much easier to demonstrate.

- Stronger customer relationships and loyalty, because borrowers who feel understood in their own language tend to come back for the next cycle and bring family with them, which compounds into a real revenue impact over a few cycles.

McKinsey's research on AI in banking operations suggests that agentic AI could unlock USD 200 billion to USD 340 billion in annual value globally in banking. Most of that value will be captured by lenders who operationalise agentic AI around their actual customer, not around a generic global template.

Conclusion: The Next Gold Loan Differentiator Is Language, Not Just Speed

For a decade, gold loan lenders competed on turnaround time. The next decade will be won by the lenders who make borrowers feel understood, in their own language, across every channel, at every moment of the loan lifecycle. Agentic AI for multilingual gold loans is how regional NBFCs, SFBs, and co-operative banks can deliver that experience without building a call centre in every state, and how they offer support that reduces friction for the customer while still holding the line on compliance and cost.

Leverage Rezo AI for Gold Loan Servicing

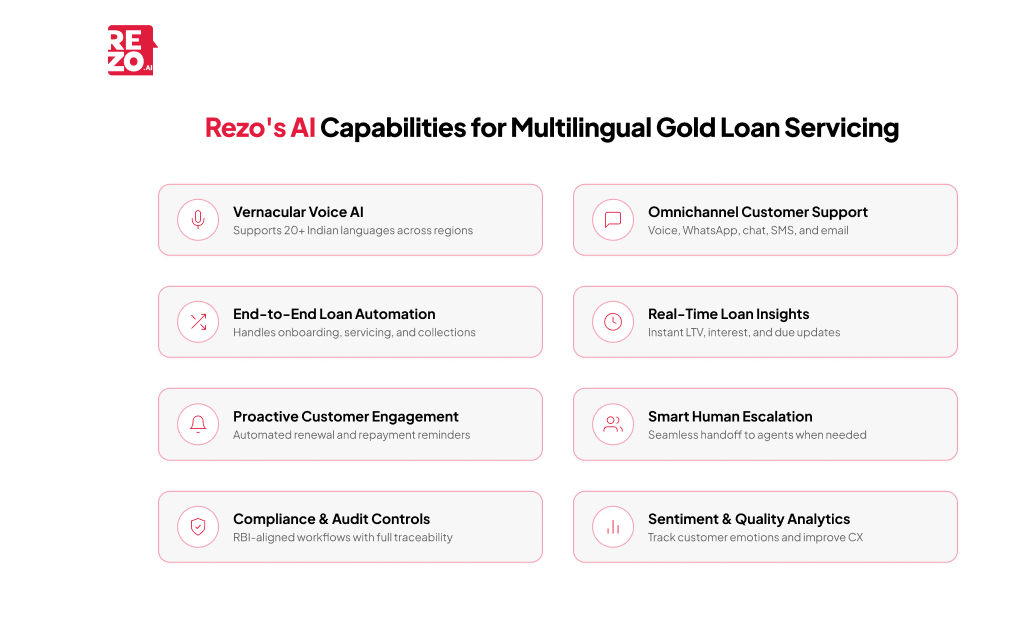

If you are exploring this shift, Rezo.ai's unified CX agentic AI platform is built for exactly this problem: voice-first, vernacular-deep, WhatsApp-ready, and designed around the way Indian borrowers actually speak and service their gold loans. The platform speaks and understands 13+ Indian languages along that borrowers use, and orchestrates a single thread across voice, WhatsApp, chat, SMS, and email so the customer is never asked to repeat themself across channels.

On the servicing side, Rezo.ai's agents handle the full gold loan lifecycle from onboarding nudges and pledge-status queries to renewal and top-up outreach, LTV-triggered conversations, EMI reminders, partial-release guidance, auction notices, and grievance intake, with a clear handover path to branch staff or tele-callers when a conversation needs a human. Under the hood, the platform plugs into existing LOS, CRM, and telephony through APIs rather than forcing a rip-and-replace, enforces RBI and Fair Practices Code guardrails such as consent, call-window, and frequency controls automatically, and ships every interaction with searchable multilingual transcripts, sentiment scoring, and a quality-analyst console so compliance and CX teams actually see what is happening. For regional NBFCs, co-operative banks, and small finance banks, that is how a gold loan book grows in five languages at once without hiring a separate call centre for each.

Frequently Asked Questions

Is agentic AI safe for handling sensitive gold loan customer data?

Yes, when deployed on an enterprise platform with role-based access, encryption in transit and at rest, India-based data residency, and full call and chat audit trails. Regional lenders should insist on SOC 2 or equivalent certifications and RBI-aligned data handling before go-live.

Can agentic AI support gold loan customers who switch between languages mid-call?

Yes. Modern conversational AI is trained on code-mixed speech such as Hinglish, Tanglish, and Manglish, so it can follow a borrower who moves between a regional language and English within the same sentence without losing context. The system also detects the customer's language automatically from the opening message, so no one has to navigate a language selection menu.

How long does a regional NBFC usually take to go live with multilingual agentic AI?

A focused pilot on one flow and two languages typically goes live in six to ten weeks, including LOS and LMS integration, QA setup, and compliance sign-off. Scaling to more languages and use cases happens in phased waves after the first flow is stable.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now