How AI Is Transforming Gold Loan Collections in India

How AI Is Transforming Gold Loan Collections in India

India runs on gold. From wedding gifts to emergency savings, gold has been woven into the financial fabric of millions of households for generations. And today, that cultural affinity has powered a gold loan market worth ₹11.8 lakh crore as of March 2025, with ICRA projections pushing it toward ₹15 lakh crore by March 2026. But here is the other side of the story: as gold loan portfolios have expanded rapidly, debt collection is struggling to keep up. Artificial intelligence is stepping in to change that, and the transformation is already underway across NBFCs, banks, and other financial institutions in India. What was once a reactive, manual process is becoming a proactive, data-driven system powered by AI tools that can operate at a scale no human team could match.

Why Gold Loan Collections Need a Rethink?

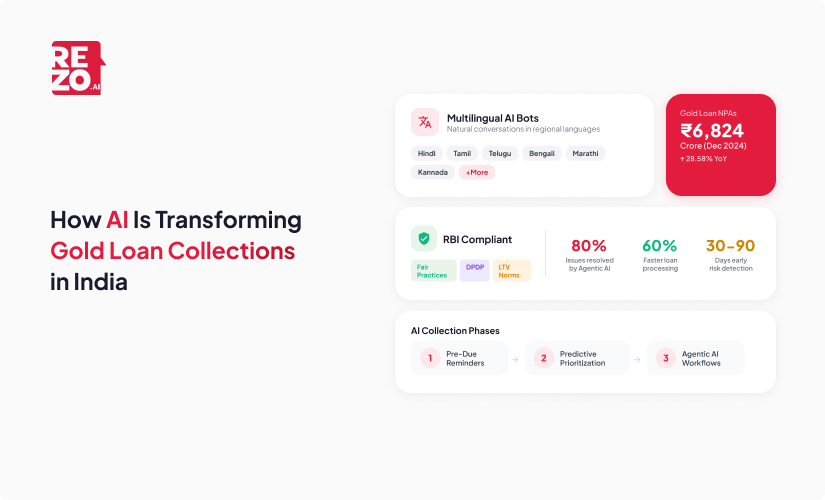

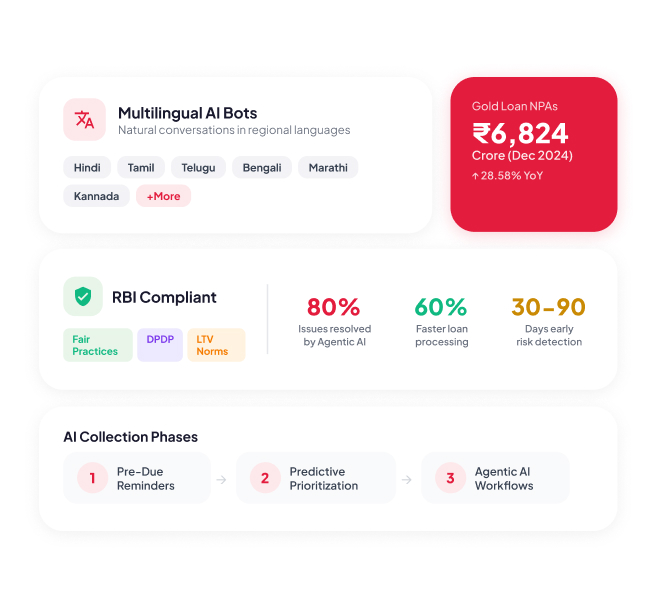

The gold loan market's rapid growth has brought a not-so-golden problem. NPAs (Non-Performing Assets) from gold loans surged to ₹6,824 crore by December 2024, a staggering 28.58% increase year-on-year. For NBFCs alone, gold loan NPAs stood at ₹4,784 crore, signaling a systemic challenge that manual debt collection processes simply cannot address at scale.

Traditional methods were built for a different era. When your gold loan portfolio was concentrated in a few urban branches, a collections department making phone calls could manage debt recovery reasonably well. But today's gold loan landscape looks very different. Borrowers are spread across thousands of towns and villages, speaking different languages, loan ticket sizes are smaller but volumes are exponentially higher, and the regulatory bar for fair collection practices has never been higher.

The math is simple: the old way of doing debt collection does not scale with a market growing at over 50% year-on-year. For the debt collection industry at large, something has to change, and that something is artificial intelligence.

What Makes Gold Loan Collections So Challenging?

Gold loans are not like personal loans or credit card debt. They come with their own set of debt collection complexities that make traditional approaches fall short.

- Customer Challenges: India's gold loan borrowers are spread across geographies, languages, and literacy levels. A farmer in rural village and a trader in a metropolitan city need entirely different service approaches. Language barriers cause misunderstood terms, geographic remoteness limits branch access, and low financial literacy means customers often don't fully grasp interest structures or default consequences creating risk for both borrower and lender.

- Trust & Emotional Sensitivity: Gold in Indian households is inherited, emotionally significant, and rarely pledged lightly. Borrowers handing over jewellery need constant reassurance around safety, insurance, and transparency. Any communication gap especially around auctions feels like a personal betrayal, not a business transaction. Trust, once broken, spreads fast in tight-knit communities.

- Seasonal Repayments: Seasonal repayment patterns add another layer. Many gold loan borrowers, especially in rural India, are tied to agricultural income cycles. Payment behaviour and cash flow fluctuate with harvest seasons, monsoon quality, and gold price movements. A rigid debt collection schedule misses these nuances entirely.

- High Volume of Interactions: Volume versus capacity creates a bottleneck. A typical collection agent handles 80 to 100 calls per day, much of which is spent on repetitive tasks like multiple call attempts and chasing unresponsive accounts. When your overdue portfolio runs into lakhs of accounts, that is nowhere near enough. Meanwhile, a large share of borrowers simply ignore calls from unknown numbers, making right party contact rates even harder to improve.

- High Operational Costs: Operational costs eat into recoveries. Between salaries, office space, telephony infrastructure, data entry, and supervision, manual collection operations can consume 15 to 20% of recovered amounts. For a sector already dealing with thin margins on small-ticket loans, this is unsustainable.

How AI Is Solving These Collection Challenges

AI is not just automating calls. Artificial intelligence is fundamentally rethinking how gold loan debt collection works, from who gets called first to what language the conversation happens in and when the best time to reach out is. By leveraging data from borrower profiles, payment histories, and real-time market signals, AI tools are enabling financial institutions to optimize contact strategies and transform every stage of the debt recovery process. The introduction of AI in gold loan lending has also led to a significant reduction in approval times, with average processing speeds reportedly improving due to the automation of document verification and KYC processes.

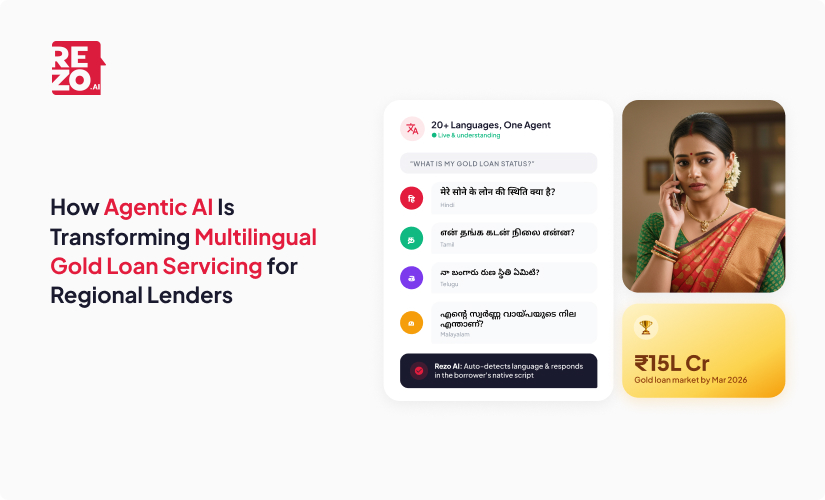

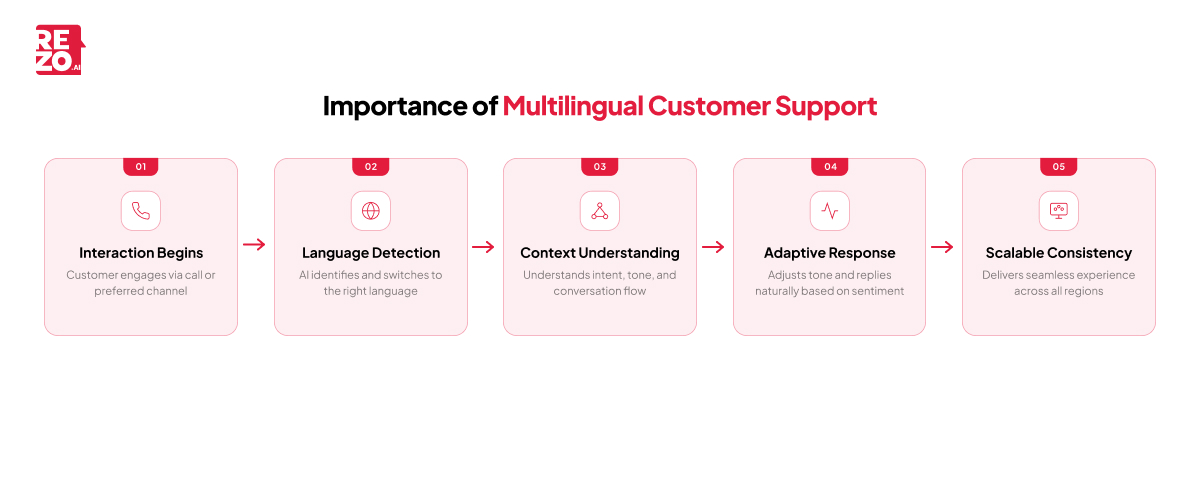

Multilingual AI Voice Bots That Actually Understand Borrowers

The most visible transformation is happening through AI-powered voice bots that can conduct natural customer interactions in Indian languages. These are not the robotic IVR menus of the past. Modern AI tools use natural language processing and sentiment analysis to understand borrower intent, detect emotional cues during customer communication, respond contextually, and adapt their tone based on the conversation flow. This level of personalized communication was previously impossible at scale.

The impact is immediate. Because these bots operate 24/7, borrowers receive automated communication immediately after a missed payment, dramatically improving collection outcomes. Auto-scheduled outbound calls trigger based on business events like pre-due dates, missed EMIs, or delinquency stage transitions. And unlike human agents, the AI voice bots maintain perfectly consistent customer interaction across every single touchpoint, delivering an enhanced customer experience even during sensitive collection conversations.

For gold loan NBFCs operating across multiple states, this means a single AI system can handle debt collection in all the regional languages (Tamil, Hindi, Marathi, Bengali, Telugu, Kannada and more) without maintaining separate language-specific teams. AI technologies like real-time sentiment analysis also help identify when a borrower is distressed, enabling the system to adjust its approach and improve customer satisfaction.

Also read: Multilingual Customer Support: The Complete Guide for Global CX Leaders

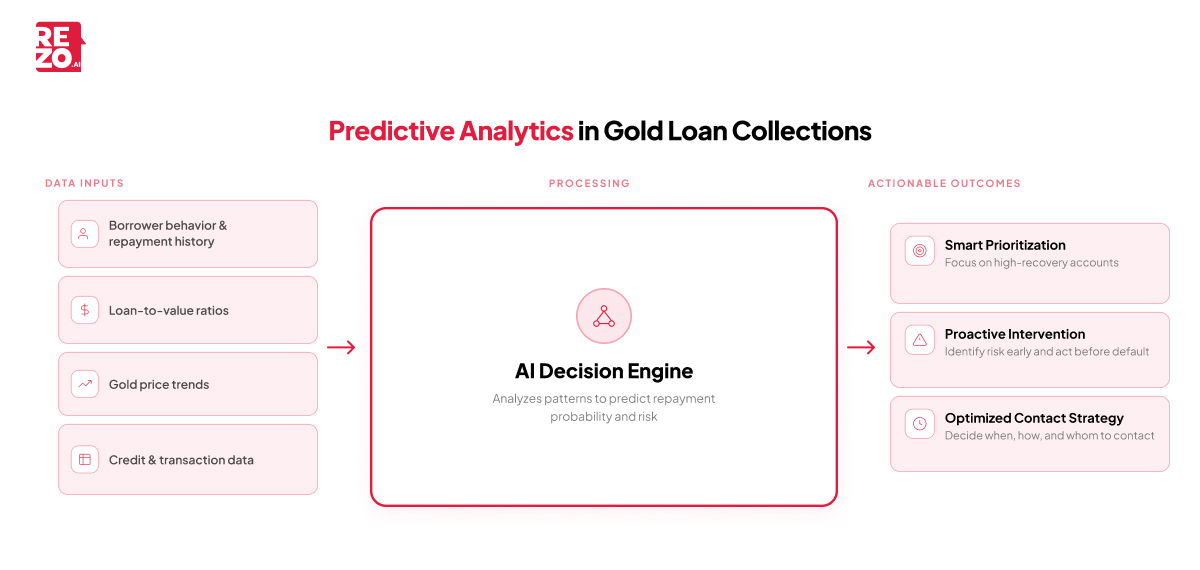

Predictive Analytics for Smarter Prioritization

Not every overdue account carries the same risk or the same recovery potential. AI-driven predictive analytics and machine learning models assess repayment probability by analyzing patterns in borrower behaviour, loan-to-value (LTV) ratios, gold price trends, credit scoring histories, and historical payment data. These machine learning models evaluate account-level data points to score delinquent accounts by collectability, allowing the collections department to focus on high-propensity-to-pay accounts first.

This means collection teams (both human and AI agents) can focus their energy where it matters most through intelligent account prioritization. High-risk accounts get immediate attention for debt recovery, while accounts with strong repayment probability but temporary cash flow issues can be supported with timely reminders and even proactive financial guidance. By evaluating thousands of accounts, predictive models can identify borrowers at risk of becoming delinquent 30 to 90 days in advance, enabling proactive outreach and intervention before a missed payment escalates into an NPA. The result is higher recovery rates with fewer touchpoints and smarter decision making across the entire portfolio.

Also Read: Predictive Customer Support: How Agentic AI Is Revolutionizing CX Automation

Agentic AI That Acts, Not Just Assists

The newest frontier in AI-powered debt collection is agentic AI, systems that do not just analyze or recommend but autonomously execute end-to-end collection workflows. Gartner predicts that agentic AI will autonomously resolve 80% of common customer service issues without human intervention by 2029.

In gold loan debt collection, AI agents can automatically identify overdue accounts, initiate contact through the borrower's preferred channel (voice, WhatsApp, SMS) in their preferred language, negotiate payment plans, send payment links, and escalate complex issues to human agents only when genuinely needed. These AI agents can also orchestrate field collection vendors, auto-assigning accounts to the best-performing agents for specific regions and loan types. AI technologies further enable lenders to create more accurate risk profiles by aggregating alternative data sources, improving lending decisions and helping reduce default rates. By automating routine tasks and enabling smarter account prioritization and personalized communication, AI platforms free collection teams to focus on hardship cases and complex negotiations where empathy and judgment matter most.

For debt collection operations running on thin margins, this shift from human-first to AI-first is a game changer that delivers measurable improvements in recovery rates, operational efficiency, and customer satisfaction.

Also Read: AI in Debt Collection

How AI Keeps Collections RBI-Compliant

For any BFSI enterprise, compliance is not optional. The RBI's Fair Practices Code lays down strict rules on how borrowers can be contacted during the debt collection process, and compliance violations carry serious reputational and financial consequences. It also mandates clear transparency and disclosure, ensuring that borrowers fully understand their loan agreements, including interest rates, terms, and conditions, communicated in a language they are comfortable with. In the context of gold loans, this extends to adherence to prescribed LTV ratios, clear communication around what constitutes a default, and a well-defined auction process in case of non-repayment.

This is where AI actually outperforms human agents in risk management. AI collection systems can have the RBI's Fair Practices Code and DPDP (Digital Personal Data Protection) principles hard-coded into their algorithms, ensuring complete compliance across every interaction. Automated workflows further ensure that all collection practices consistently adhere to regulatory guidelines set by the Reserve Bank of India. Call window restrictions are automatically enforced, and outreach is conducted in the borrower’s preferred language, maintaining clarity and respect. Every customer interaction is recorded and time-stamped for audit trails, while communication remains professional and consistent, eliminating the risk of aggressive or harassing recovery practices. Real-time compliance monitoring through AI dramatically reduces violations, translating into significant savings by minimizing fines, legal fees, and reputational damage.

With the RBI releasing comprehensive Master Directions in June 2025, consolidating over 30 scattered gold loan circulars into one unified framework, having AI systems that can be updated centrally to reflect new compliance requirements is a significant operational advantage. Financial institutions that leverage AI for compliance can continuously monitor regulatory changes, ensure adherence to evolving norms such as LTV limits and borrower communication standards, and adapt their processes without the lag that comes with retraining hundreds of field staff.

What Does Implementation Actually Look Like?

For Heads of Collections, CX leaders, and CIOs evaluating AI adoption, the most common question is: where do we start? Implementing AI successfully requires a phased approach, and the most successful lending operations follow a clear roadmap.

Phase 1: Start with pre-due reminders and early-stage delinquency.

This is the lowest-risk, highest-volume use case. AI voice bots handle routine tasks like reminders and initial outreach across the portfolio, freeing human agents for complex cases. Automated workflows ensure all debt collection practices adhere to regulatory guidelines from day one. Most enterprises see measurable results within 60 to 90 days.

Phase 2: Expand to mid-stage debt collection with predictive prioritization.

Once the AI system has enough data from Phase 1, predictive models start segmenting borrowers and recommending the most effective contact strategies. AI-powered collections platforms enhance right party contact rates and ensure compliance while improving debt recovery. This is where recovery rates typically see the biggest jump.

Phase 3: Integrate agentic AI for autonomous workflows.

The final stage brings end-to-end automation with intelligent escalation. AI agents handle 80% of routine collection interactions, including negotiating payment plans, sending payment reminders, and managing follow-ups, while human agents focus exclusively on hardship cases, disputes, and complex negotiations that require human review.

The hybrid model is key. This is not about replacing collection teams. It is about giving them AI-powered leverage so they can focus on the 20% of cases where human judgment and empathy genuinely matter.

Integration with existing CRM, loan origination systems (LOS), and telephony infrastructure is essential. AI solutions built for loan processing and debt collection plug into your current stack rather than requiring a complete overhaul, making implementing AI far less disruptive than many financial institutions expect.

Key metrics to track:

- connect rates

- promise-to-pay conversion rates

- cost per recovery

- average resolution time

- compliance audit scores.

These real time insights help collections teams continuously monitor performance and refine their approach.

What the Future Holds for AI in Gold Loan Collections

The trajectory is clear, and the acceleration is only beginning. Several future trends and market trends point to AI becoming indispensable for gold loan lending operations.

The RBI's new LTV norms (85% for gold loans up to ₹2.5 lakh, effective April 2026) will make gold loans more accessible, supporting financial inclusion and affordable credit for underserved borrowers while expanding portfolios further. This makes AI-driven debt collection even more essential. The global market for AI-driven loan origination is projected to grow exponentially, signalling that the industry is firmly embracing AI as the foundation for modern financial operations.

Omnichannel collection strategies represent an emerging technologies frontier where AI orchestrates outreach seamlessly across voice calls, WhatsApp messages, SMS, and email, meeting borrowers on whichever channel they prefer and building stronger customer relationships through consistent, personalized communication. AI-driven collections platforms further enable teams to prioritize accounts more effectively, enhancing right-party contact (RPC) rates while ensuring adherence to regulatory frameworks. Real-time gold price monitoring linked to automated LTV alerts will enable proactive debt collection interventions before accounts become delinquent. AI technologies also enable lenders to create more accurate risk profiles by aggregating alternative data sources, supporting better-informed lending decisions and helping reduce default rates. AI tools with fraud detection capabilities add another layer of risk management, flagging suspicious activity across the loan processing chain.

As of 2026, enterprises globally have already deployed generative AI in at least one business function, the question for Indian NBFCs and banks is no longer whether to adopt artificial intelligence in customer service and debt collection but how fast they can do it. Early adopters are already seeing the competitive edge, and those deploying AI-driven solutions across their collections department are pulling ahead. The AI revolution in debt recovery is not coming. It is here, and why AI matters for the future of gold loan collections has never been clearer.

Conclusion

Gold loan debt collection in India is at an inflection point. A market growing at breakneck speed, rising NPAs, evolving RBI regulations, and borrowers spread across the length and breadth of the country demand a fundamentally different approach. AI-powered voice bots, predictive analytics, machine learning, and agentic AI agents are not futuristic concepts. They are operational AI tools already delivering measurable results in recovery rates, compliance adherence, decision making, and cost efficiency.

For financial institutions serious about transforming their gold loan debt collection, the playbook is clear: start with high-volume, low-complexity use cases, scale with AI-driven contact center operations, and move toward autonomous collection workflows that leverage AI at every stage. Implementing AI across debt recovery operations is no longer a question of if but when. The technology is ready. The market is demanding it. The only question is whether your collection operations will lead the transformation or be left catching up.

Frequently Asked Questions

Can AI predict gold loan defaults before they happen?

Yes. Predictive AI models analyze repayment patterns, transaction history, gold price fluctuations, credit scoring data, and borrower financial behaviour using real-time data to flag at-risk accounts early. By assessing multiple risk factors, these predictive models can identify accounts at risk of becoming delinquent 30 to 90 days in advance. This allows financial institutions to intervene proactively with reminders, payment plans, or restructuring options before a missed payment becomes an NPA, strengthening both debt recovery outcomes and customer experience.

How do AI voice bots handle regional languages during gold loan collection calls?

Modern AI voice bots use advanced natural language processing to conduct conversations fluently in Indian languages, including Hindi, Tamil, Telugu, Bengali, Marathi, Kannada and more. They detect the borrower's language preference automatically and adapt tone and phrasing for natural, culturally appropriate customer interaction. These AI technologies also enable instant approvals of language switching mid-conversation, ensuring every borrower receives a seamless and inclusive lending experience regardless of their region or dialect.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now